Wondering how the PC gaming market managed to achieve its highest ever revenues in 2023? Our global pc market report 2024 unveils the driving forces behind the growth as well as industry trends that will guide the market in the next 5 years.

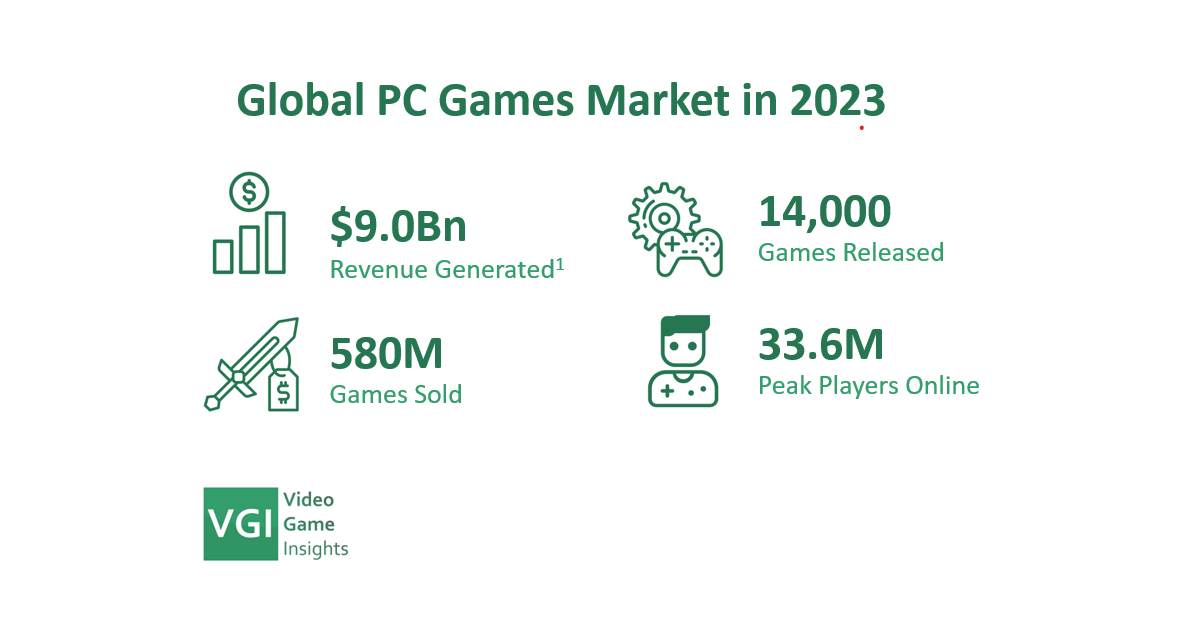

The PC market set records in 2023 with highest ever revenues, units sold, peak players online and number of games released on Steam.

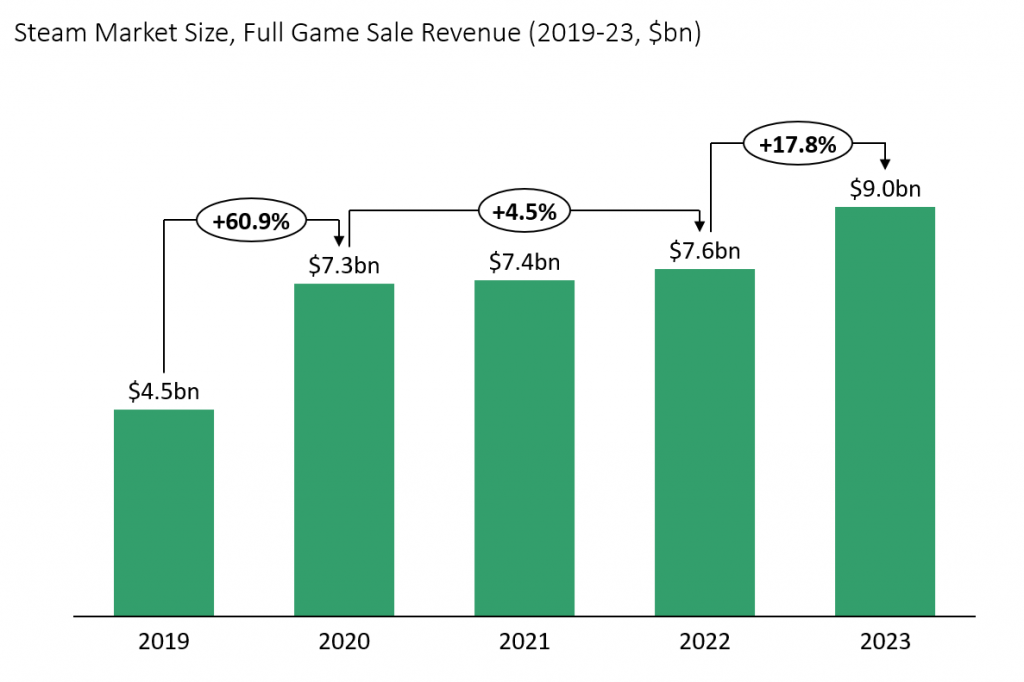

2023 saw over $9bn gross full game revenue generated on Steam with 580 million game copies sold and about 14,000 new games released.

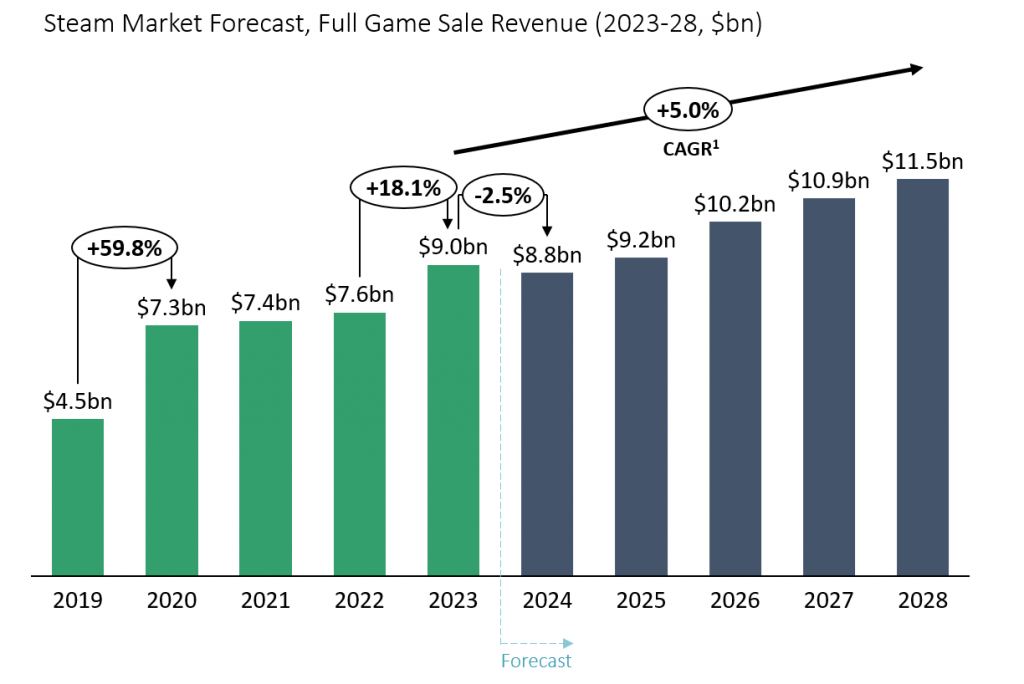

Total gross revenue from game sales (excluding microtransactions) grew by 17.8% in 2023. This comes after several years of flat revenues as the games industry was recovering from the COVID boom.

PC games market will continue to grow at approximately 5% per year for the foreseeable future. However, 2024 is expected to be a down year. A weaker slate of new releases, combined with an exceptional 2023, makes it challenging to forecast growth for 2024, despite some positive tailwinds.

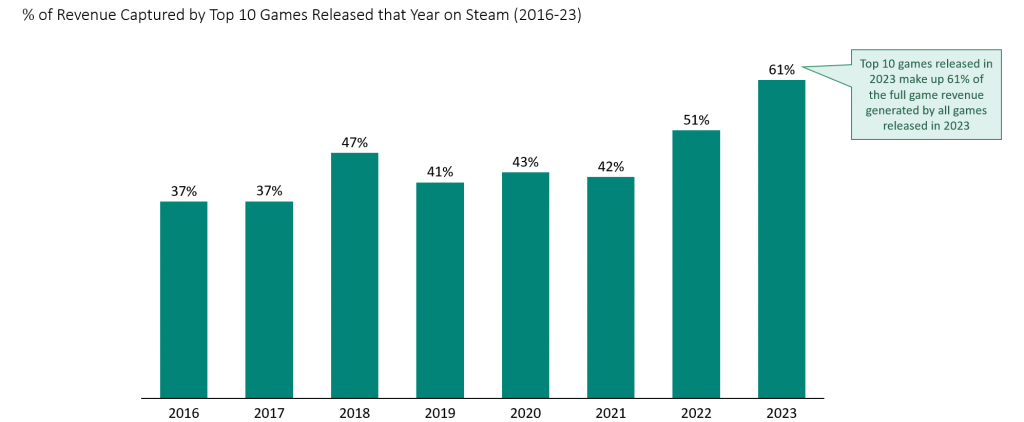

The PC games industry has become increasingly “winner takes it all” over the last 8 years. Top 10 releases of 2023 made up 61% of the total revenue generated by new releases.

Steam covers vast majority of the PC market these days and the trends on Steam are broadly reflective of other, much smaller PC games stores. Therefore, our report is largely based on Steam data.

Video Game Insights is not affiliated with Steam or Valve and all data provided is estimates.

Explore our platform to learn more

Video Game Insights is powering the creativity in the games industry through data. We provide free articles and market reports as well as a comprehensive data and intelligence platform for developers, publishers and investors. Use the menu on the left to explore our tools or search for any game or games company in the search bar above.

Steam has been hitting records across many metrics as we’re entering the holiday period. Full Game revenue for 2023 has already beat last year’s and we’ve still got a busy month ahead.

Black Friday performance is no exception. A year of strong game releases tied to unprecedented attractive promo deals has pushed 2023 Black Friday to highest units sold ever.

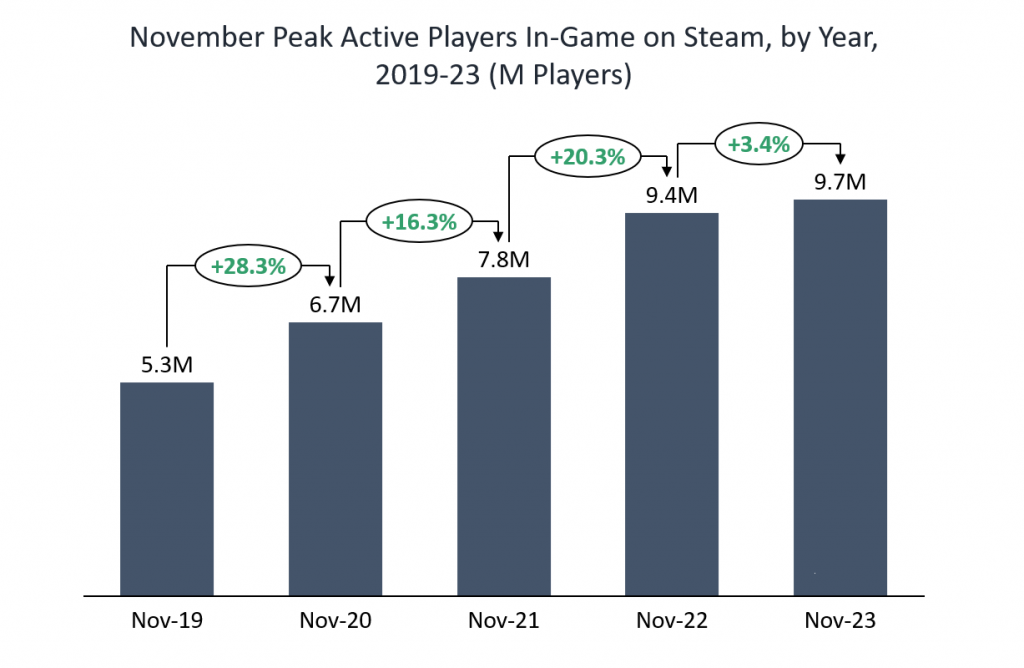

User engagement keeps breaking records on Steam despite the post-covid normalization

Covid helped to boost the whole games industry with people stuck inside and nothing better to do. New people picked up gaming as a hobby and old gamers had more time to game. The post-covid world has been tough for the games industry – years of growth that culminated with a peak in 2020 have turned to stagnation and even decline.

The exception to this has been the PC gaming space where Steam has continued to hit new record levels of engagement. Peak active users have continued to push past the Covid peak of April 2020.

The Black Fridays are no exception – 2023 November saw another record in terms of peak active players in-game on Steam.

However, this growth in engagement has clearly slowed. In fact, 2023 November peak was only 3.4% higher than last year’s.

At least partly, availability of the next generation of consoles can be blamed for this slowdown. It’s been 3 years since PlayStation 5 and Xbox X were released, but it wasn’t till 2023 that the supply really started to catch up with the demand. People who had to substitute their preferred console for PC are now able to return to… well, let’s be serious – to PlayStation.

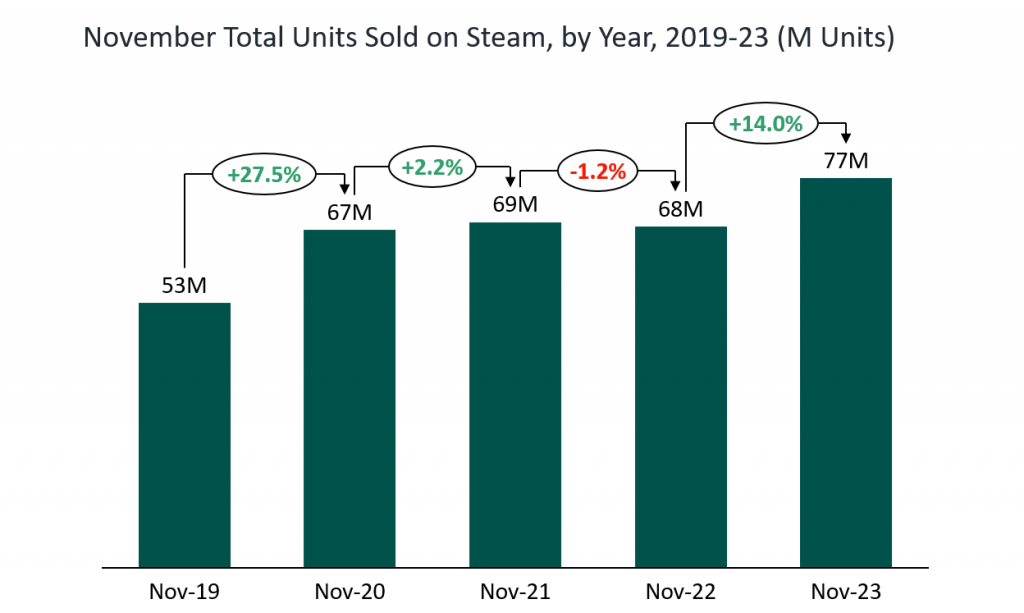

2023 is a year of significant growth after the stagnating Black Friday sales on Steam in 2021-22

Even though engagement continued strong on Steam, units sold have stagnated since 2020. Players had a large library of existing games to play and new releases were underwhelming or delayed.

2023 broke that with a strong release slate. While some of these anticipated releases underperformed expectations (Starfield, anyone?), others beat even the wildest of predictions (Baldur’s Gate 3).

This has resulted in the strongest ever Black Friday sales on Steam, beating 2022 by 14%.

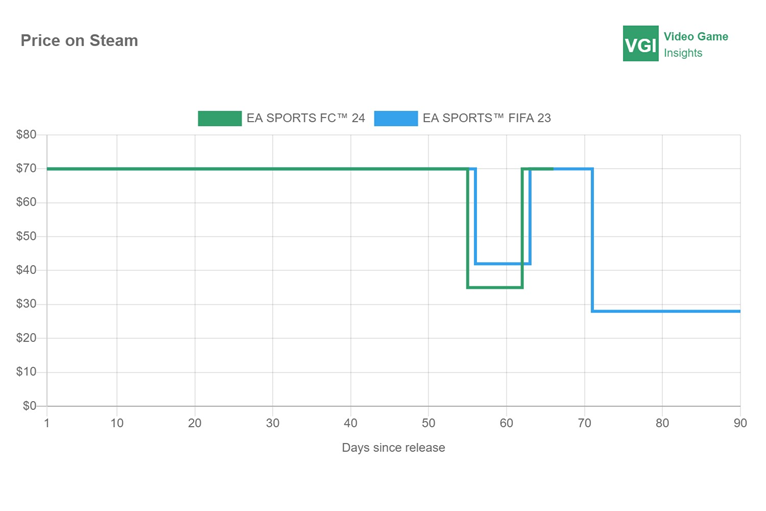

Deeper discounts were the first tool to be used by publishers in the fight for limited attention

2023 has been a tough year for many publishers as the market is getting increasingly saturated and new player growth has slowed. A natural response to that has been discounting more to boost visibility and discoverability.

EA Sports FC was on 50% sale across all platforms less than 2 months after release – the steepest ever promo for them.

Other big name 2023 releases have also gone as far as 40% off less than a year since release. Although not atypical for large titles, the amount of discounted big releases still played a role during the Black Friday.

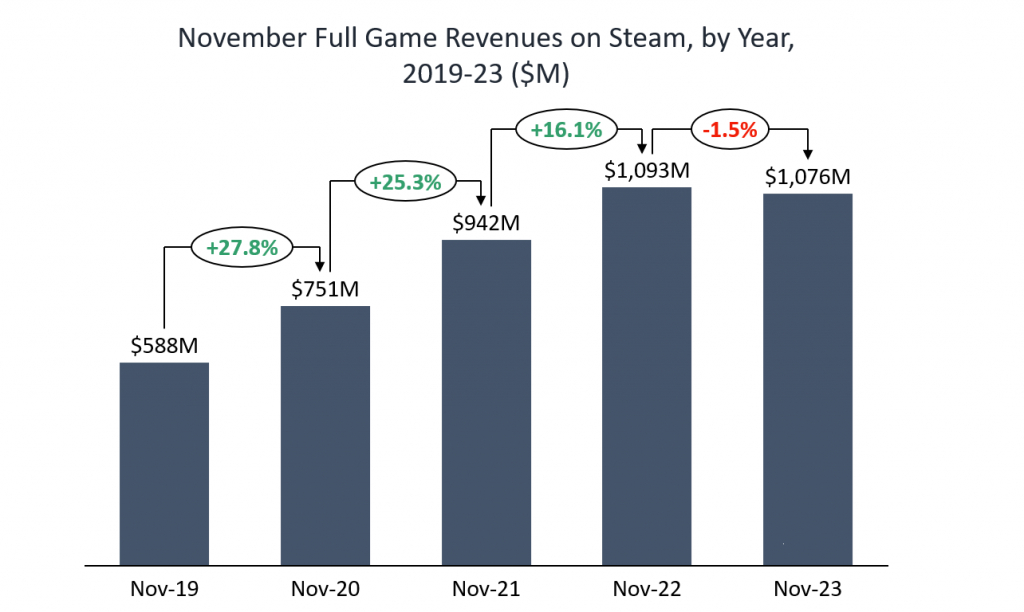

Slightly declining Black Friday revenue is a sign of fiercer competition among publishers for an increasingly fixed size of the pie

Higher engagement and record units sold failed to translate into higher revenues during Black Friday.

In fact, while units were up +14% YoY, full game revenue was down -1.5%. This was largely driven by steeper than usual discounts boosting units, but at lower average selling price. Players’ overall lower disposable income this year and higher competition between games due to strong releases has led to a push to the bottom as publishers are fighting for attention

Price pressure likely to continue as the games industry is facing increased supply and peaking demand

The decline in average game selling price is likely to continue as several games industry dynamics push the prices to the same direction:

Subscription platforms such as Xbox Game Pass are likely to continue to offer great value for money in the coming years with many day 1 releases appearing free on the platforms

Economic downturn is affecting consumers’ disposable income, leading to a decrease in spending on non-essential items, including video games. Publishers are already responding by offering more discounts to maintain sales volume

Slowdown in gamer growth is a global trend as Covid pulled many gamers to be forward. The markets that continue to grow tend to be more price sensitive. The new users that aren’t already gamers tend to be more casual, also pushing down spend

Increased competition between publishers on the ultra-premium games side. Many AAA publishers have adapted the same strategy of fewer, but higher quality games released

Lower costs on indie studios through easy-to-use game engines like Unreal Engine 5 and AI support in asset creation helps small teams to create increasingly complex games, increasing the overall supply of good quality games

Longer and more replayable games have been a trend for many years now. However, the evergreen nature of some of these games is creating a dynamic not seen in the games industry before where new releases compete for attention with games that are over 10 years old

The pressure to discount sooner and deeper will be good for gamers in the short term. However, the increased pressure on studio margins will likely result in more redundancies, streamlining and efficiency, which ultimately might not be the right formula for best games.

Steam continues to reach new highs despite the overall games industry facing post-covid headwinds.

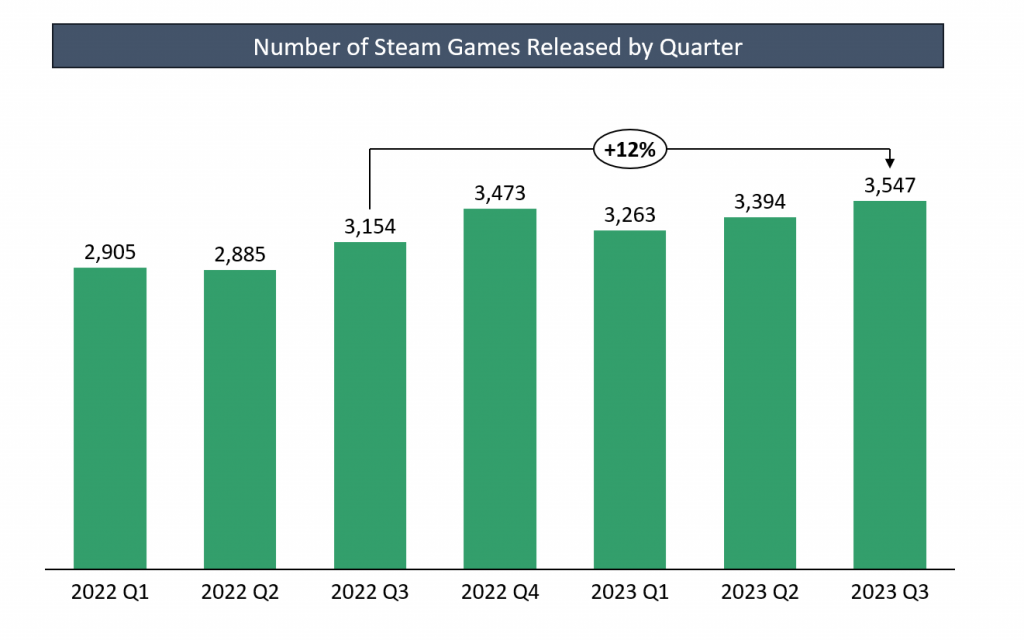

Q3 2023 saw Steam beat records in terms of new games released, total units sold as well as full game revenue.

3,547 new games released on Steam

3rd quarter of 2023 saw a whopping 3,547 new games released on Steam. This is more than the previous record of 3,473 in Q4 2022. It’s also 12% more than same time last year.

However, AAA & AA games only saw 38 new games released, a -13% YoY decline. Growth in new games releases continues to be led by small hobby developers and indie studios.

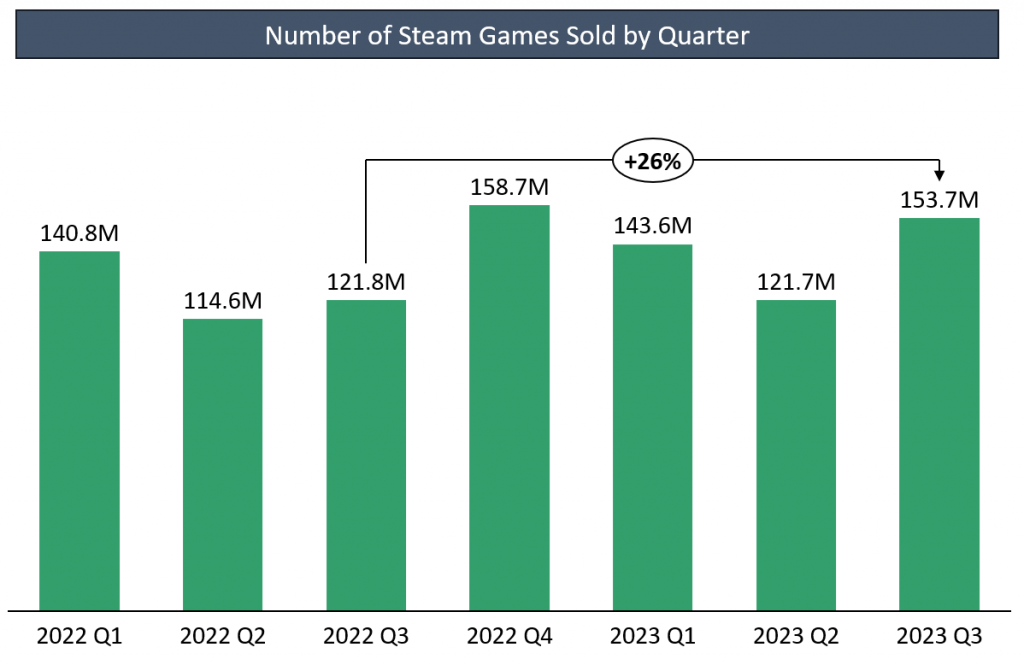

1.7 million games sold on Steam per day

Steam saw 154 million game copies sold in Q3 2023. This is +26% more than last year. Although strong performance, it falls short of the traditionally strongest Q4 performances, driven by Black Friday and Holiday sales.

Strong Q3 unit sales were largely driven by strong AAA launches. Baldur’s Gate 3 & Starfield dominated the premium game sales while Overwatch 2 and Counter-Strike 2 helped to boost free to play game installs.

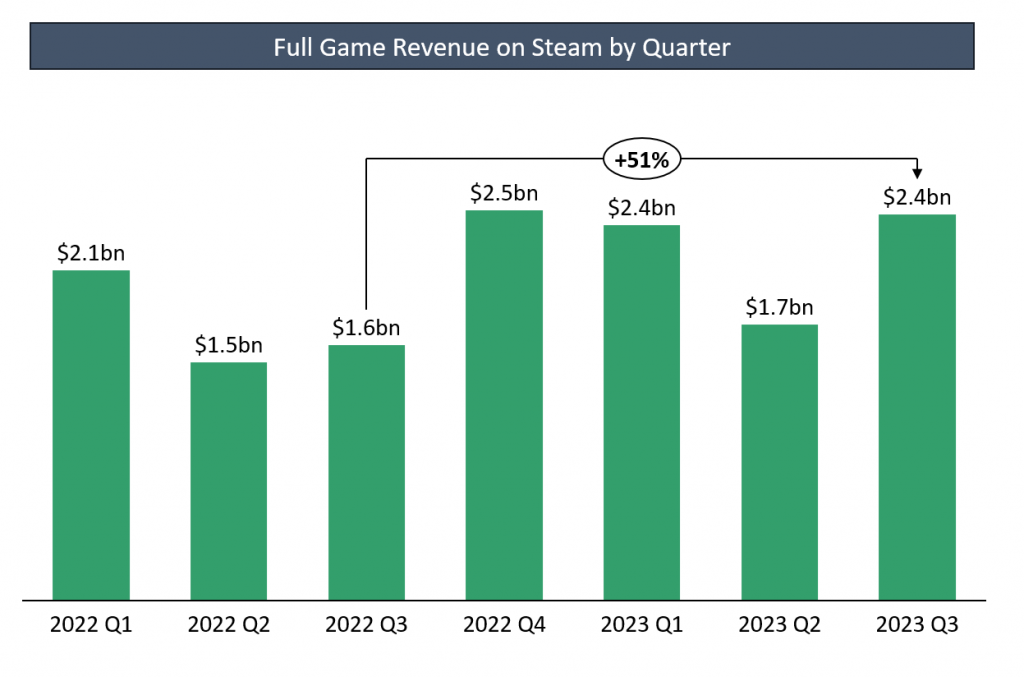

Over $2 billion in full game revenues

Q3 2023 saw $2.43bn in full game revenues on Steam, up +51% YoY. Q3, traditionally one of the weaker quarters as a result of steep sales, saw a big boost, driven by new game launches, selling at full price.

AAA & AA games made up $1.8bn or 74% of all Q3 revenues and grew by +74% YoY.

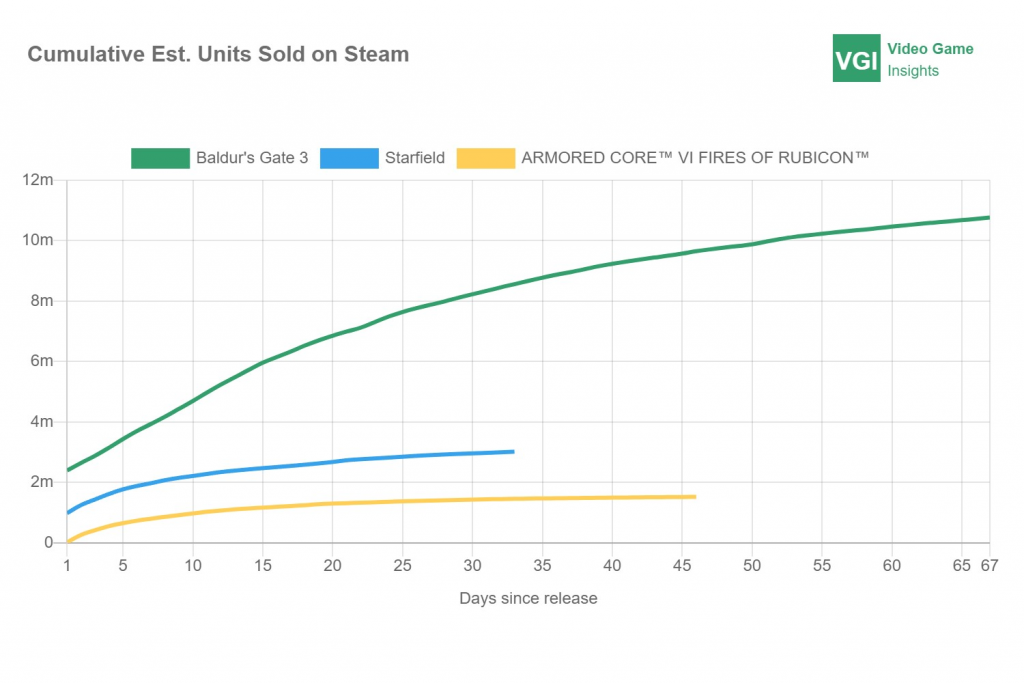

The domination of Baldur’s Gate 3

Baldur’s Gate 3, Starfield and Armored Core VI were the top 3 biggest releases of Q3 2023. However, there was really only 1 massive hit in that period – Baldur’s Gate 3.

With over 10 million units sold in the first 2 months, Baldur’s Gate 3 overshadowed all other releases by a wide margin.

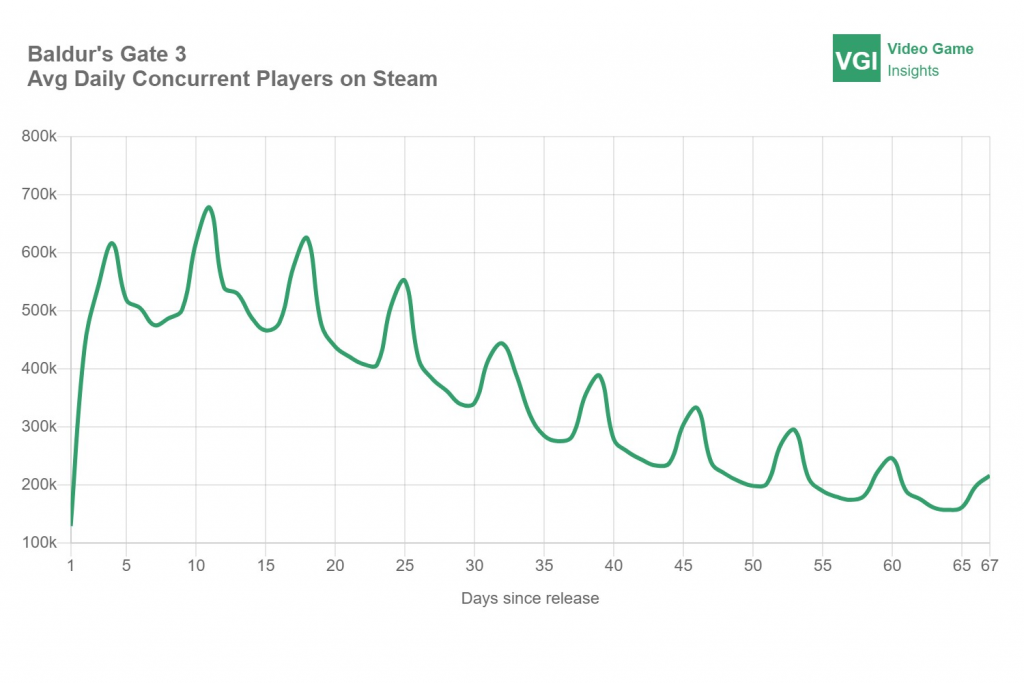

Even 2 months after launch, there are c. 200k people playing the game at any given time

Leading up to a strong year for Steam games in 2023

Steam market is on track to generate over $9bn in full game revenue in 2023, a strong +18% growth over 2022.

This is a welcome sign of strength in the PC market. Steam saw a strong revenue growth in 2020. However, 2020-22 were fairly flat as a result of post-covid normalization and weaker consumer spend.

2023 shows that major AAA hits can still deliver growth in the industry, boosting revenues to new highs.

This article explores the average selling price for Steam games. It is important to differentiate between

base price – the original price set for the game and average selling price – the true price people paid for the game, including things like promotions

The analysis below includes the average selling price and takes into consideration promotional sales.

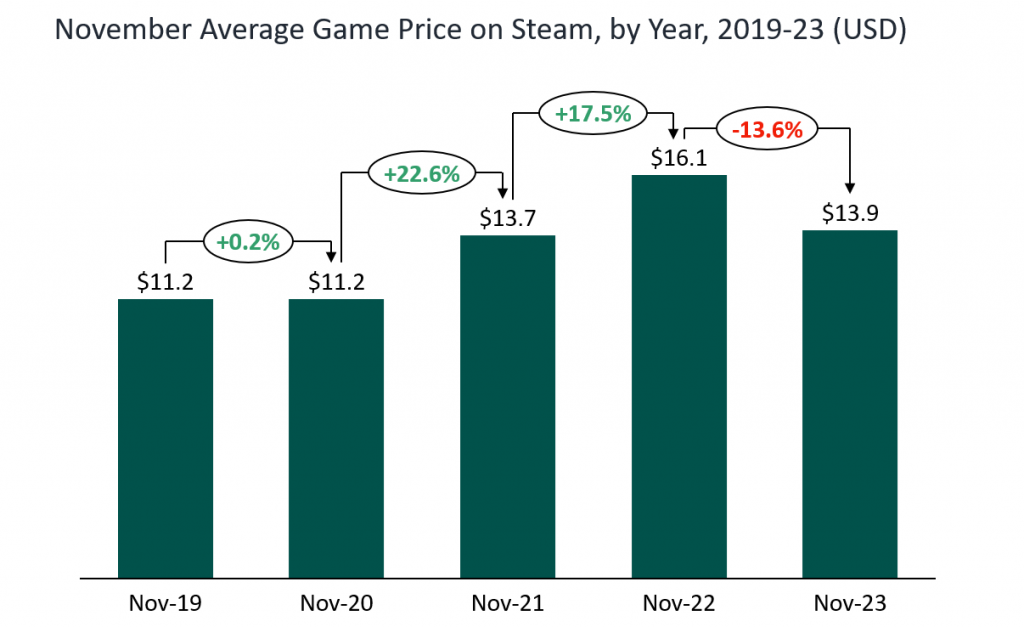

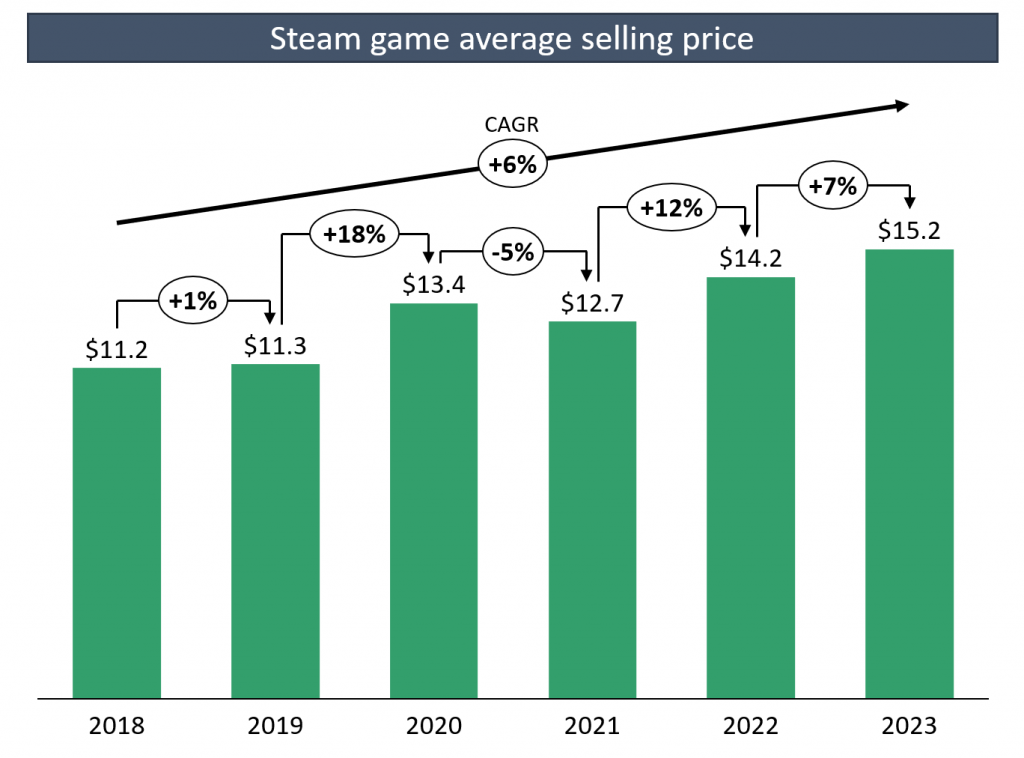

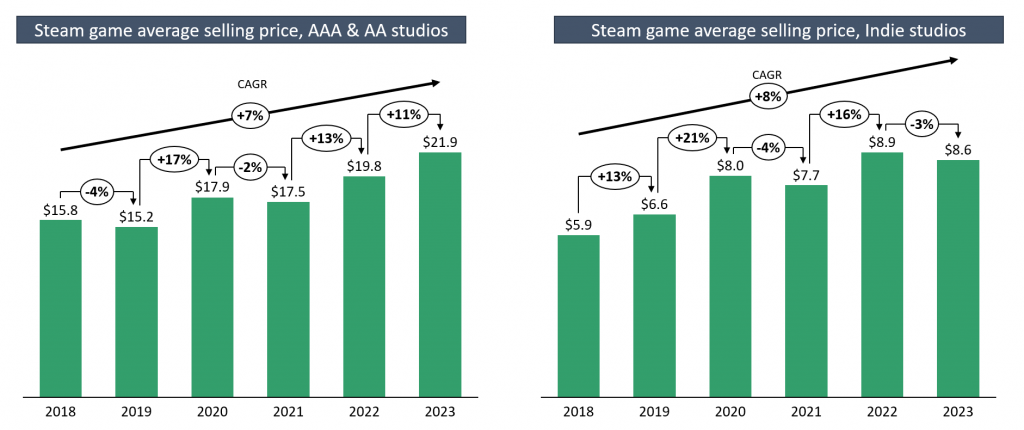

Players are willing to spend more than ever – what recession?

Our analysis shows that the average price paid per game on Steam has increased from $11 in 2018 to $15 in 2023. That is, on average, 6% growth per year. Inflation in the US in the same period has been c. 4% per year. So video game prices seem to have outpaced general inflation.

The biggest price jump happened in 2020, as COVID boosted both engagement, but also players’ willingness to spend on video games.

2021 saw some normalisation in games prices, but the prices have continued to grow since then.

This increase in prices is likely mostly driven by players purchasing more expensive games, rather than buying at lower discount rates. Many publishers have moved their default game price up from $59.99 to $69.99 in that time period as well as pushed their B tier games to be priced at more expensive price points.

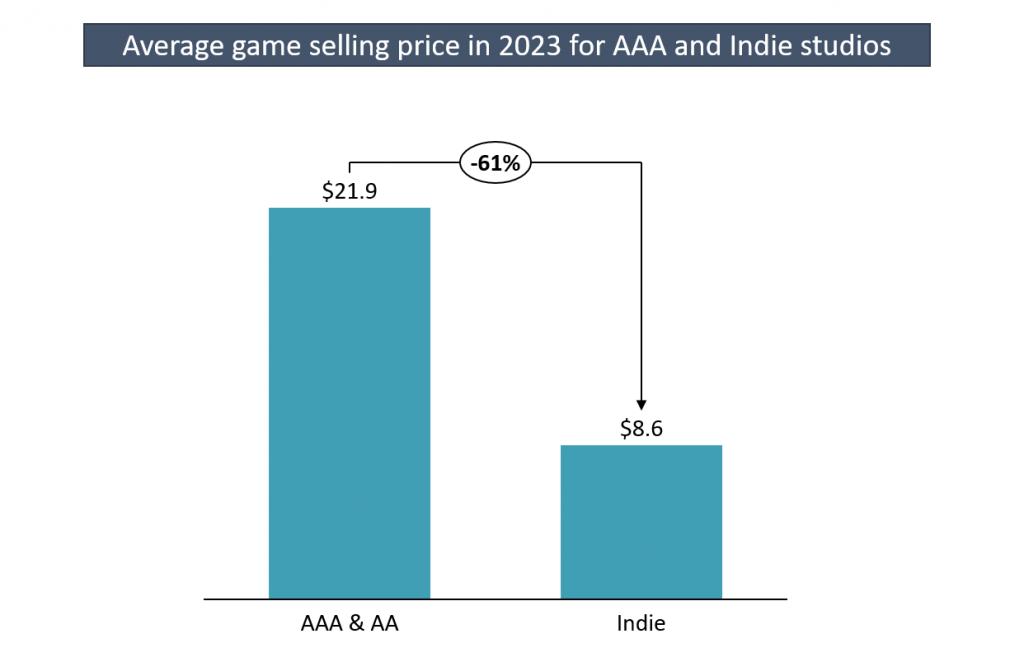

Indie studios continue to see significantly lower average selling prices

Indie games sell, on average, at 61% discount VS their AAA counterparts.

Of course, indie games tend to be much lower budget games. That also tends to be reflected in the base price. The original base prices for indie games are, on average, 63% cheaper VS AAA to begin with. The fact that the promo price adjusted average prices are similarly lower indicates that there is no substantial difference in indie VS AAA games promo strategies.

Large and small studios see a divergence of price increase in 2023

Historical pricing trends for large and small studios have been very similar. Both have seen large positive COVID impact to pricing as well as some normalisation in 2021.

However, 2023 has seen an 11% price increase for AAA and AA games as a result of some larger game releases that have driven up prices.

At the same time, indie studios’ average price has decreased by -3% year over year. This comes at a time of high inflation, putting extra pressure on smaller studios and their ability to monetise the games.

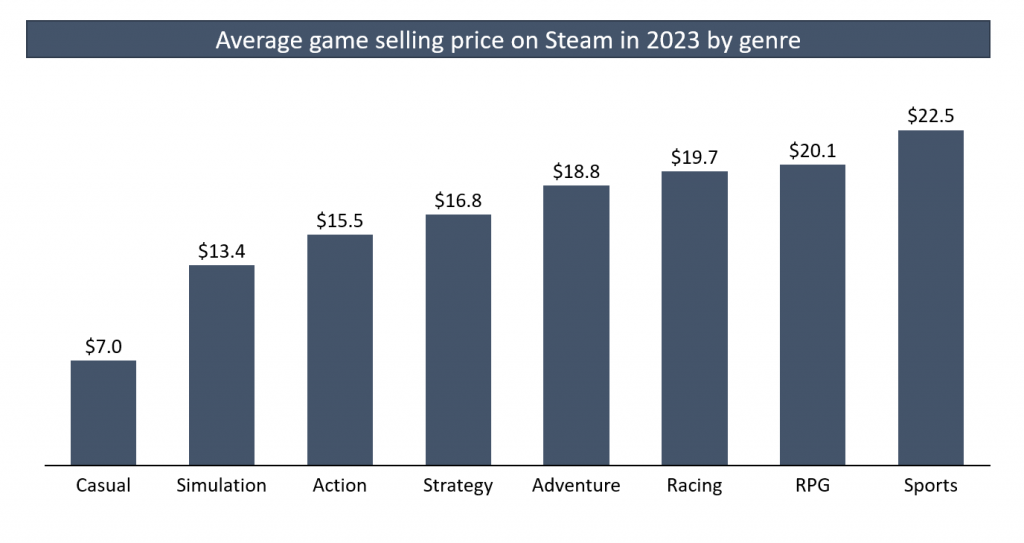

Some genres attract higher prices than others

Key highlights on pricing differences by genres

Sports and racing genres tend to sell at higher prices than other games. Their player base tends to be different to typical hardcore Steam players. The players tend to be more tied to the specific sport or race as fans and, therefore, willing to pay higher prices and wait less for steep discounts.

Action and adventure games see the highest variability of prices within genre. Large AAA games like CoD continue to attract players at high price points while smaller studios have to come in at much lower prices to compete with the mega-budget games.

Casual games continue to be in their own category, with many games being free to play or priced at $1.99. This category most resembles mobile games and their business dynamic.

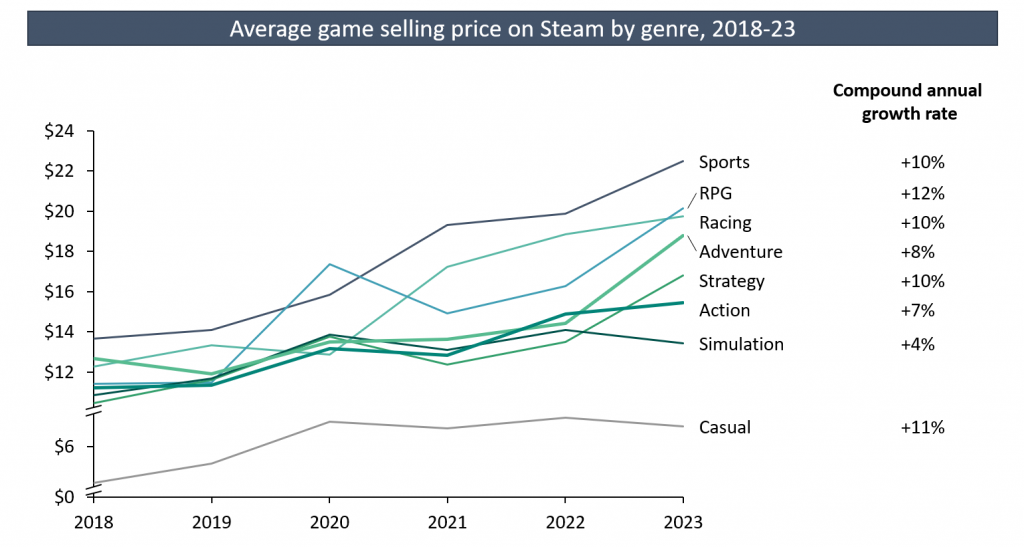

All genres have seen price growth in the recent years

Key highlights on pricing differences by genres over time:

Most genres have grown their average selling prices by over 10% a year in the last 5 years.

Simulation games have grown less than others. This might be driven by an increased amount of lower tier simulation games being released on Steam.

RPG games have seen the highest increase, though that is largely driven by some major RPG releases in 2023.

Casual games saw a large structural shift in price during COVID and have stayed fairly flat since then.

Steam market continues to be healthy

Steam market has continued growing in 2023. Overall price is up 7%, but total untis are also up year over year. Engagement data, including concurrent users on Steam and in-game continue to beat records quarter after quarter.

We’re able to see the full impact of Covid to the PC games industry now, 3 years after the start of the pandemic.

We can clearly see how different the Covid experience has been to small and nimble indies, the middle-market developers and the AAA giants of the games industry.

But first, let’s see what the PC games landscape looks like in general.

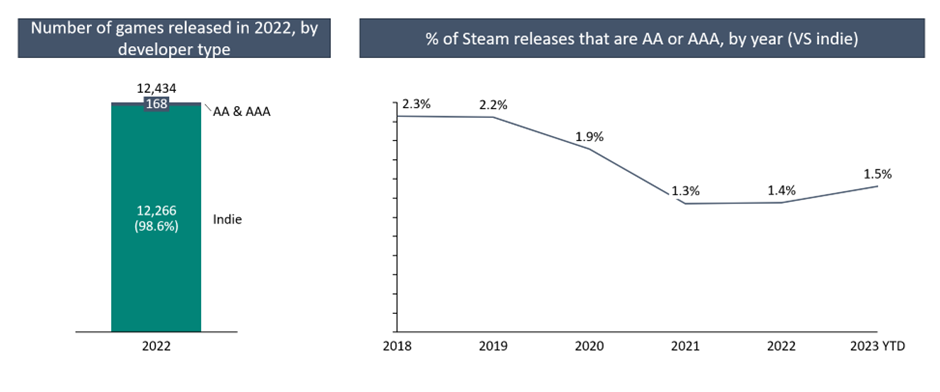

Indie games dominate new releases

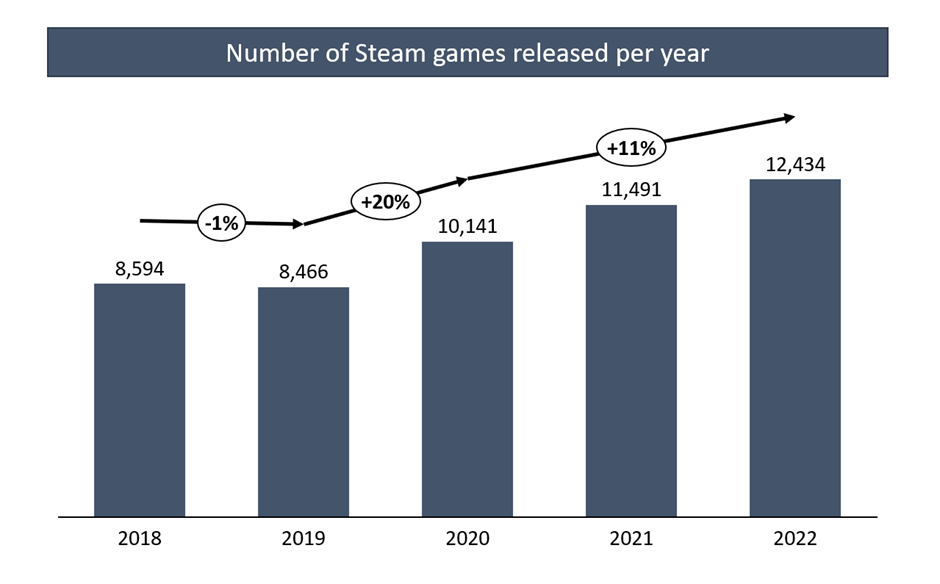

Steam sees thousands of new games added on the platform every year, vast majority of them indie games. Out of the 12,434 games released in 2022, 99% were indies.

As a side note, indie studios tend to be small & independent game developers. This can range from a 1-person home studio to 100s of people in other cases. The definitions of indie, AA and AAA are often blurred. You can read more about our definitions here.

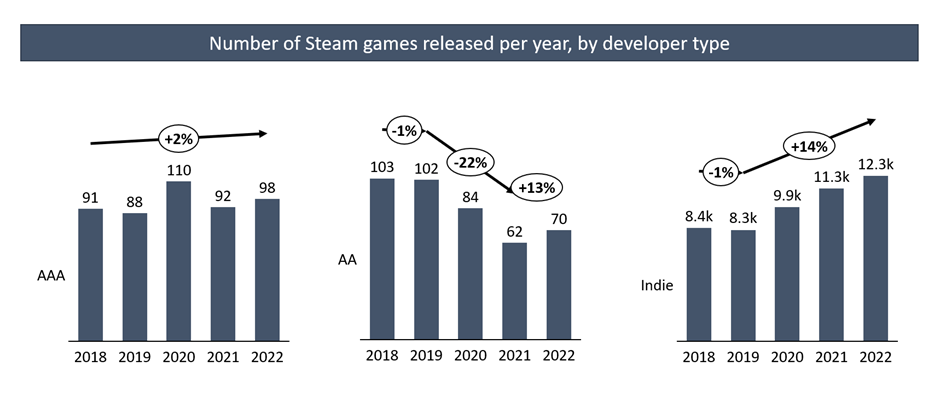

In fact, AA & AAA games made up 2.3% of Steam releases in 2018, but dropped to 1.3% during the Covid year of 2021. Large releases have recovered a bit since then, up to 1.5% in 2023, but remain below the pre-covid levels.

Overall new Steam game releases continue to grow at an accelerated pace since Covid

Pre-covid years of 2018 and 2019 saw an already large number of Steam games released annually, c. 8,500. That accelerated during 2020 as Covid allowed many people to work from home and increase their time spent on hobby projects.

The pace of new game releases has continued since 2020, reaching 12,000 new game releases in 2022 or 34 new games every day!

Flat giants, growing small studios and declining middle-market

The Steam game releases become more insightful when looking at AAA, AA and indie releases in isolation.

AAA studios were able to more or less mitigate covid impact quickly with better structured home working, better process and, let’s be honest, with some crunch. In fact, 2020 saw a record amount of AAA releases. It might be that some studios scrambled to get their game released early, in order to benefit from the Covid boost.

Indie studios have been the clear winners. Having already set up flexible working or fully remote studios meant many studios were barely impacted. Smaller hobby projects saw a huge boom as the working from home AAA and AA employees now had more time for side-projects.

AA studios were the clear losers. While pre-Covid saw c. 100 AA game released every year, this had fallen to only 62 by 2021. 2022 has seen some recovery, but it’s still significantly below pre-Covid years.

The fall of the AA games

We predict that the AA games continue to suffer, being squeezed form both sides. The c. $10-50M budget games have a significantly large cost base, but often don’t hit the critical sell-through rates.

On the indie side, Unreal Engine 5, AI and other developments have made it easier than ever for small teams to make great games, significantly increasing the B and C tier game supply.

On the AAA side, Game Pass, Epic store’s free giveaways and PS+ significantly increase the amount of “free” or cheap top tier games available to players. Players can also rely on their existing libraries of games or steep AAA discounts. The need to buy a new game at full price has taken a big hit.

It’s easy to see how macroeconomic squeeze to people’s wallets, tied to increased availability of free or cheap AAA and indie games make the “good, but not my top choice” of games struggle.

This all means that the “mid-tier” games have seen some pretty bad launches in 2022 and 2023, significantly underperforming expectations.

The recent news have highlighted Embracer closing some mid-sized studios and the underpefromance of games like Ubisoft’s Mario + Rabbids sequel or 2K’s Marvel’s Midnight Suns. Our platform also suggests some other recent launches such as F1 23 have been a lot weaker than previous iterations.

This trend is unlikely to stop in 2024 and 25. We are already seeing large studios shifting more of their eggs to larger game baskets and away from the “mid-tier”. We’re also seeing publishers like Embracer suffer, cancel games and restructure, as their focus on mid-tier hasn’t paid off.

The future is big and small, but not average

Our prediction is that big games and small studios continue to win and grow while the mid-tier of games falls out of favour for the foreseeable future.

As the innovation in game development technologies continues, it is likely that smaller indie studios will replace the current mid-tier at some point. What costs $20M to make today, might cost $5M in 5 years, making the economics much more favourable.

It looks like the pain for the mid-tier is here to stay.

Core Keeper is a sandbox survival sim that has been described as a blend of Stardew Valley, Terraria, Minecraft and Valheim. Essentially, it’s everything that Steam players love in one game.

It announced that by the end of June 2022 it had sold over 1 million units. This article explores the game’s performance as well as the reasons behind the game’s immediate success.

COVID boosted game sales across all platforms, but PC games were a strong winner. Steam games revenues grew by 31% in 2020 and a further 11% in 2021.

2022 has brought challenges to the industry. The whole industry will likely decline in 2022. Games on Steam will also see a decline, but will fare better than the rest of the industry.

Which countries dominate the Steam publishing space?

Getting a game published is hard as is. Finding out that all the publishers you’d want to get are abroad makes it even worse.

In this article we’re exploring where most Steam publishers are geographically. We’ve tagged over 2,300 Steam publishers countries. They collectively make up over 95% of the revenue on the platform.

The US tops the country list both in terms of number of publishers and by revenue they generate. However, there are a few surprising countries that make it to the top 10.

Only 10% of Steam developers have ever made more than $100k in gross revenue. This article explores what they’re doing that other developers aren’t. It covers self-publishing, genre focus, number of games developed and more.