We’re excited to announce that we are now part of the Sensor Tower family. This acquisition will allow us to significantly boost our platform offering and the speed at which we can deliver new features to our clients. Our combined gaming intelligence solutions will include PC, Console and mobile insights, providing customers with an unparalleled view of the gaming landscape.

🚀 Video Game Insights will now operate as “Video Game Insights by Sensor Tower.” 🎮 Click here to read the full announcement

We will release a lot more information about our future plans in the following weeks. Stay tuned!

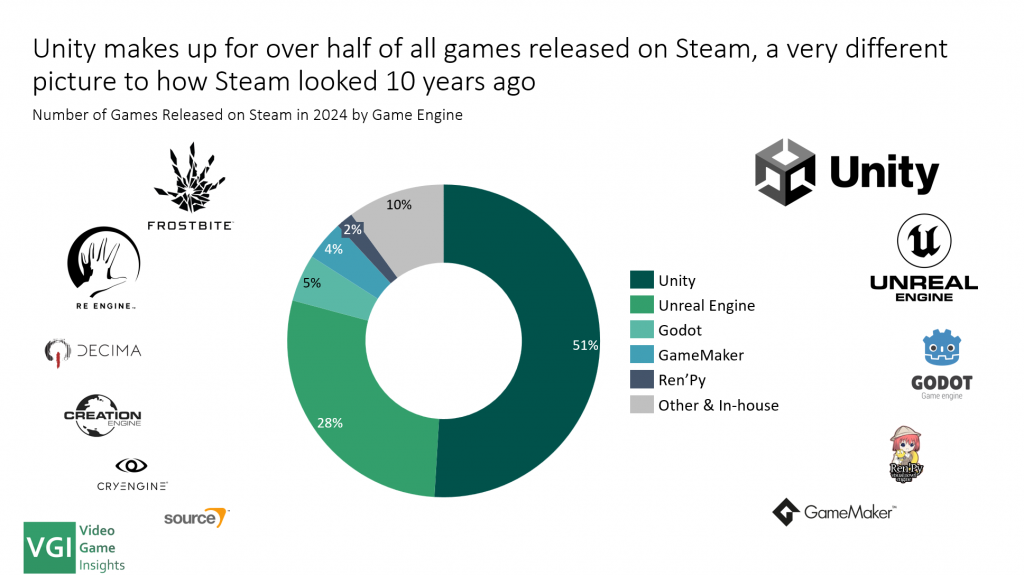

Video game engines have evolved significantly over the past decade. While mobile game development has long been dominated by third-party engines—most notably Unity—the same was not true for PC and console games.

Until recently, the majority of large titles were developed using in-house, custom-built engines. Not anymore.

This report covers:

– State of game engines today – Game engine market share trends over time – Forecasting the future trends – Did Unity’s pricing debacle impact market share? – The growth of Unreal Engine – Is Godot really winning share? – Game engine shares by sub-genre of games

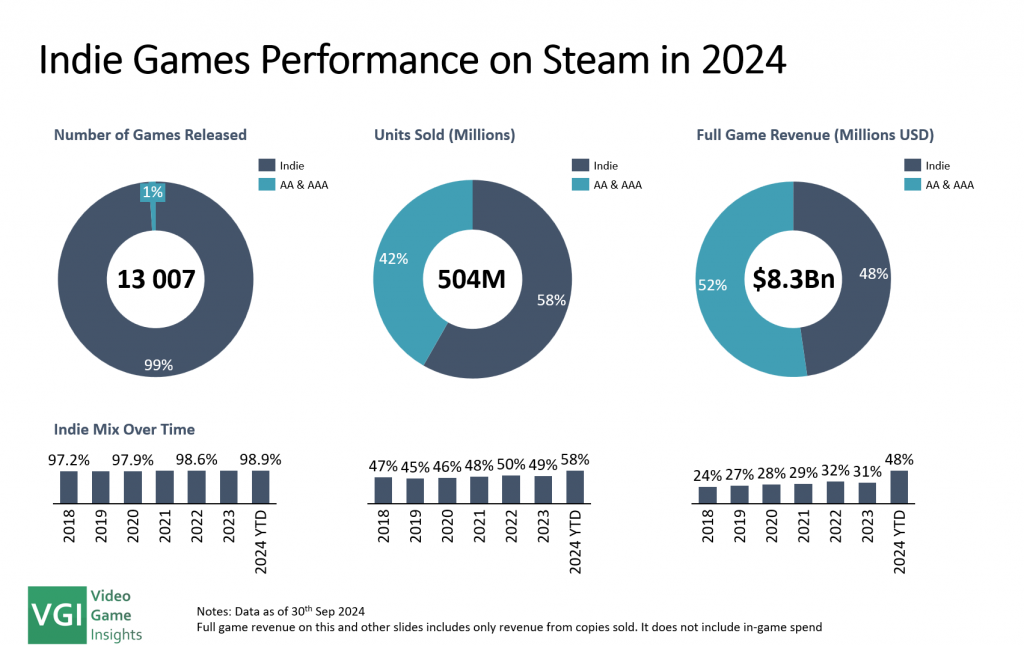

The global indie games market has hit new heights in 2024. Our Global Indie Games Market Report 2024 offers an in-depth analysis of the indie game landscape. Discover key data on market growth, top-performing games, and trends shaping the future of indie gaming.

Indie Games Now Rival AAA Titles on Steam: For the first time ever, indie games are generating as much revenue as AAA and AA titles on Steam.

Top Indie Game Releases of 2024: Black Myth: Wukong and Palworld have set new records, with tens of millions of units sold.

Growth of the Indie Market: Indie games sector has grown every year since 2020 despite the wider industry slowdown.

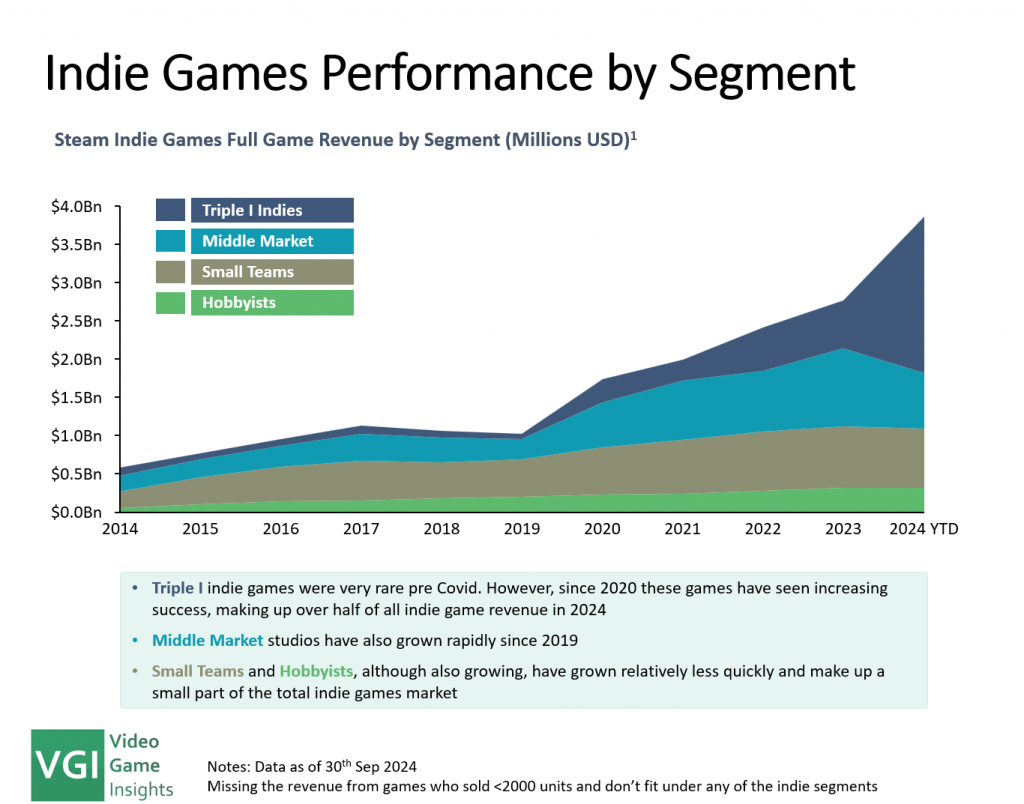

Segmenting the Indie Market: Indie market splits into Triple I Indies, Middle Market, Small Teams, and Hobbyists. Each segment has seen unique trends in the last 4 years.

Indie Studios are Maturing: More studios are releasing their 2nd or 3rd games, with experienced developers seeing better financial success with each release.

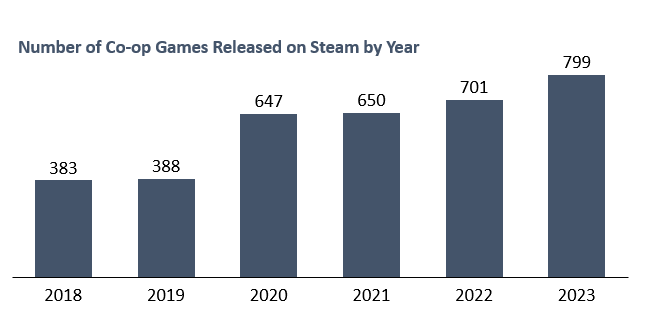

2023 saw almost 800 co-op games released on Steam, over double from five years ago.

The core principle for cooperative games is that a small group of players can work together as a team. Covid saw a peak in co-op game interest as catching up in the real world was swapped for social gaming sessions. This report explores how the co-op game popularity has trended since.

Co-op games tend to have an organic player acquisition flywheel where players persuade their friends to get the game. Therefore, co-op games tend to outperform other types of games in their performance. These organic hype cycles have become especially evident with the launches of Palworld and Helldivers 2 this year. The report looks into just how much audience attention share these games grabbed.

For many years, PlayStation has relied on platform exclusives to encourage players to buy its hardware and remain within its ecosystem. This strategy, also commonly used by Xbox and Nintendo, has been highly effective. However, since 2020, there has been a significant shift in this approach. This article explores why publishers are moving towards cross-platform strategies and examines how this shift has impacted PlayStation to date.

PlayStation’s move away from exclusivity

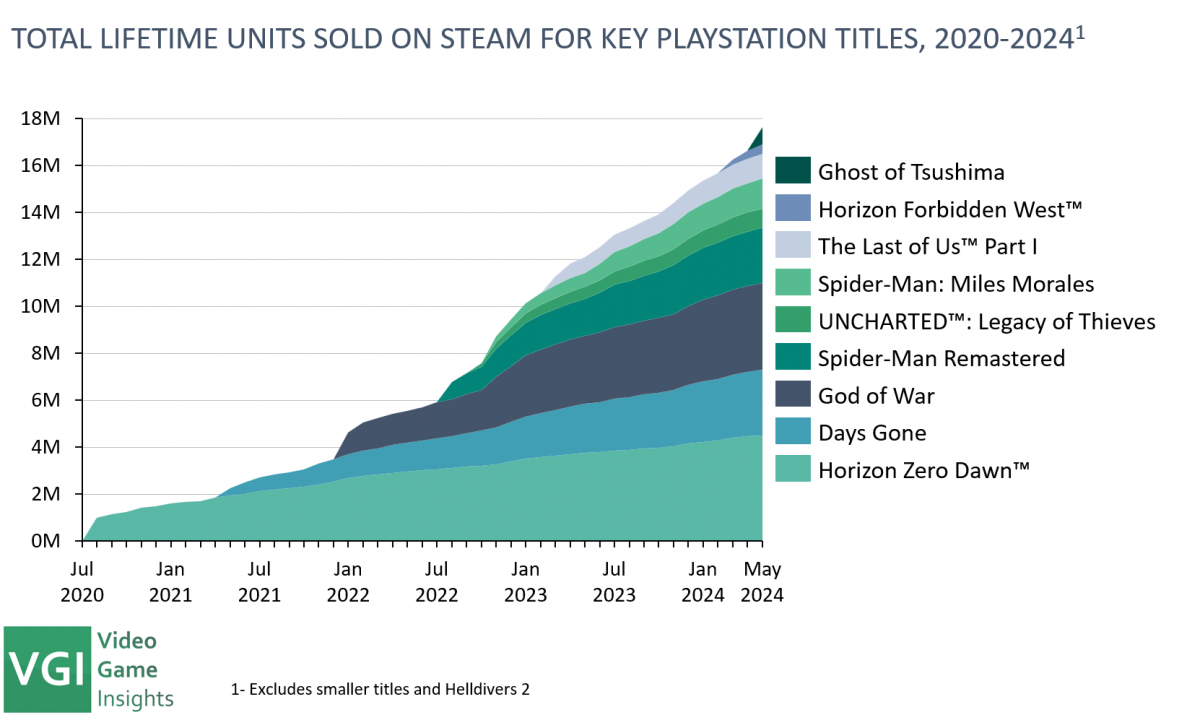

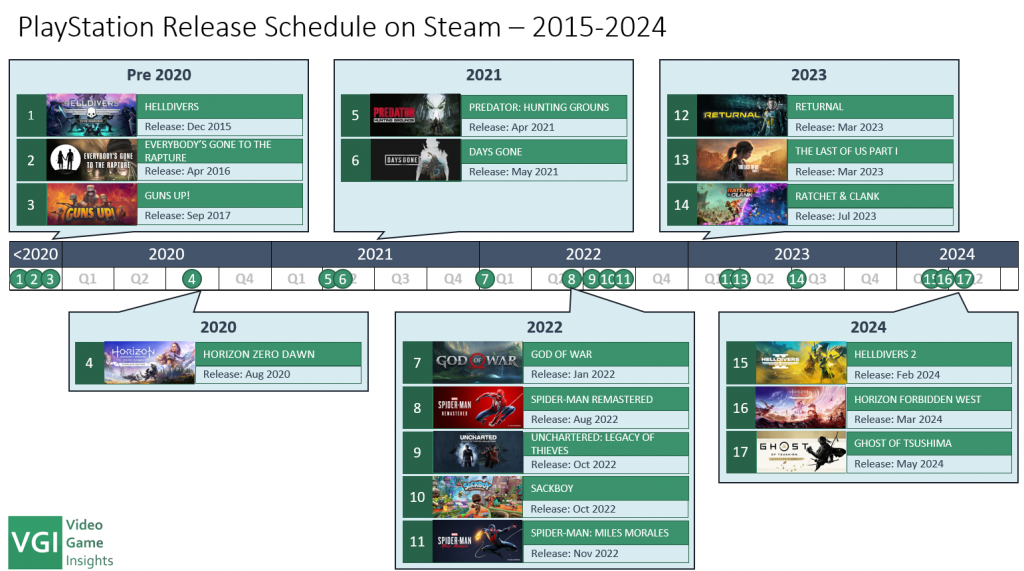

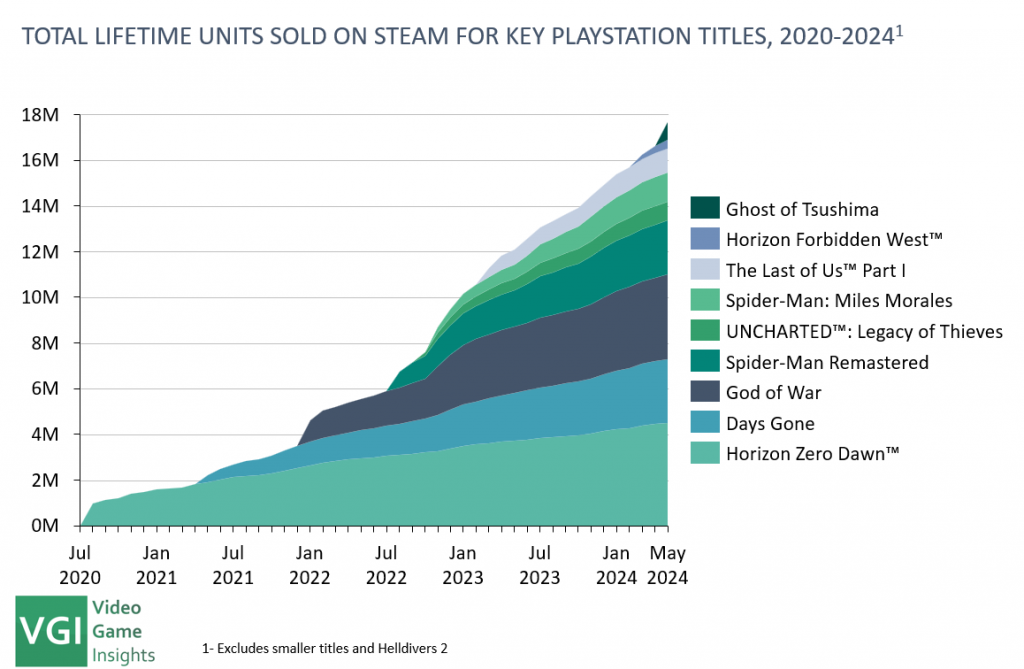

Up until 2020, PlayStation had released only three games on Steam. Their first ever game, funnily enough, was Helldivers. These initial releases were relatively minor in the grand scheme of Sony’s portfolio.

However, in August 2020, Horizon Zero Dawn was launched on Steam, marking the beginning of a significant shift. Since then, 14 PlayStation exclusives have made their way to the Steam platform.

The release strategy for these games can be categorized into three distinct approaches:

PC release approximately 3-4 years after PS release – This category includes major IPs like Horizon Zero Dawn, God of War, Spider-Man Remastered, and Ghost of Tsushima.

PC release 2 years after PS release – Titles such as Days Gone, Sackboy, Spider-Man: Miles Morales, Returnal, Ratchet & Clank, and Horizon Forbidden West fall into this category. These games are typically one tier below the top sellers and benefit from a shorter exclusivity window as their sales curves tend to flatten out sooner.

Day 1 PC & PS5 release – Live service games are released on both platforms simultaneously to maximize engagement rather than to entice PC gamers to switch to PlayStation.

In total, these PlayStation ports have sold over 17 million units on PC, excluding Helldivers 2. Including Helldivers 2, the total exceeds 28 million units (yes, Helldivers 2 is that crazy).

All unit sales estimates are derived from the Video Game Insights platform data. Although these figures are estimates, they align closely with PlayStation’s reported and leaked numbers, providing a fairly reliable approximation of actual sales.

PlayStation’s PC Porting Strategy: Three Key Aims

Maximize Launch Sales on the PS Platform: By prioritizing initial releases on PlayStation, they save the 30% Steam platform fee. More importantly, it is an important retention mechanism. This approach encourages players to stay on the PlayStation platform to access exclusives upon launch. It’s a page out of the film and TV playbook, where HBO originals debut on HBO before becoming available on other channels and platforms later.

Optimize PC sales – Therefore, PlayStation aims to launch on PC once the primary sales cycle on PlayStation’s platform concludes. Given that relatively low porting costs, sales on PC represent a high-margin opportunity.

It’s a careful balancing act to get the porting timing just right, but there are clear advantages VS a full exclusivity approach.

How the Strategy is Paying Off: The Example of Ghost of Tsushima

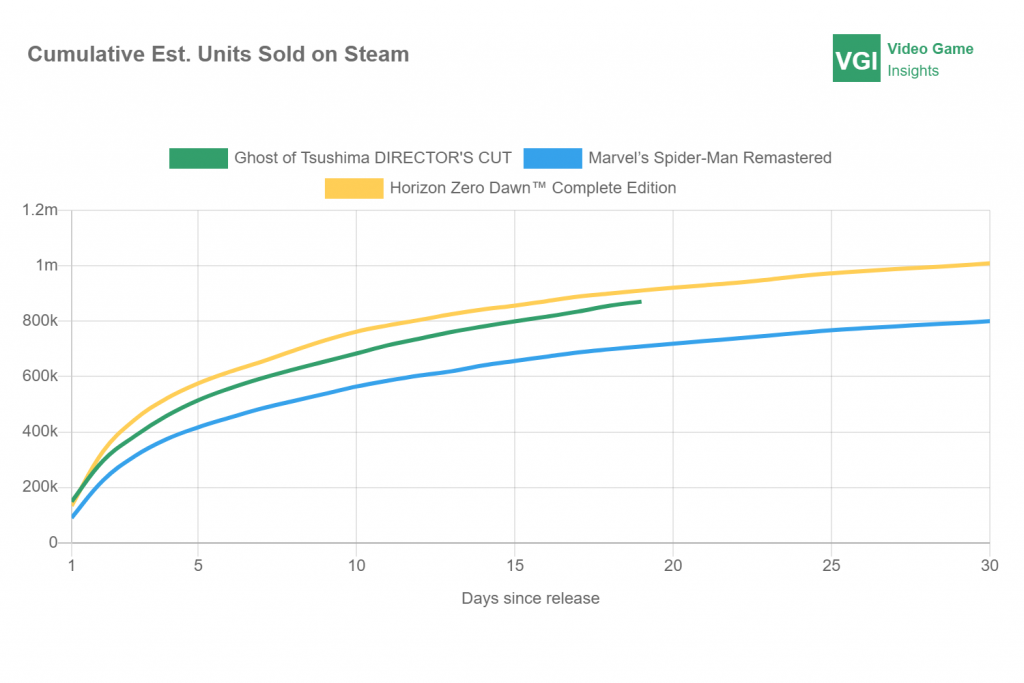

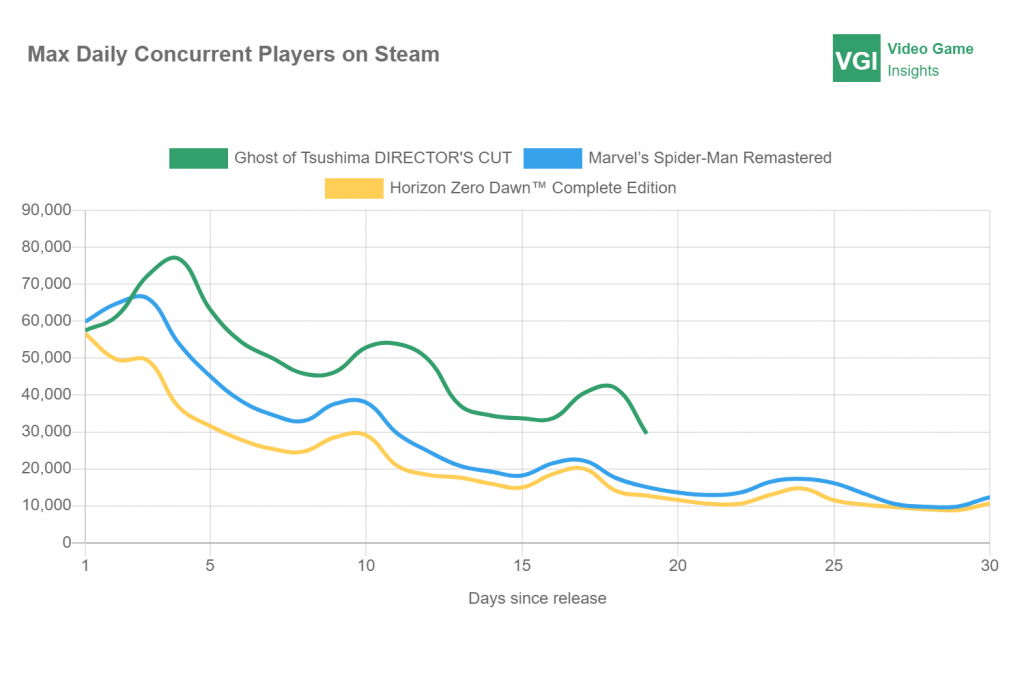

Ghost of Tsushima is the most recent example of PlayStation’s strategy, launching on Steam in May 2024, nearly four years after its original release. Its Steam debut was one of the most successful ports to date, with over 800,000 units sold in the first 20 days, comparable to the launches of Spider-Man and Horizon Zero Dawn.

In terms of player retention, Ghost of Tsushima has performed even better. While it launched with similar concurrent player (CCU) numbers as Spider-Man and Horizon, it has maintained nearly double the CCU by day 20.

While Ghost of Tsushima is a great title and well received (90% positive ratings on Steam), it’s an objectively less known IP VS Spider-man and Horizon. Ghost of Tsushima sold well on PlayStation but didn’t get close to the other two. So, what made its launch so successful on Steam?

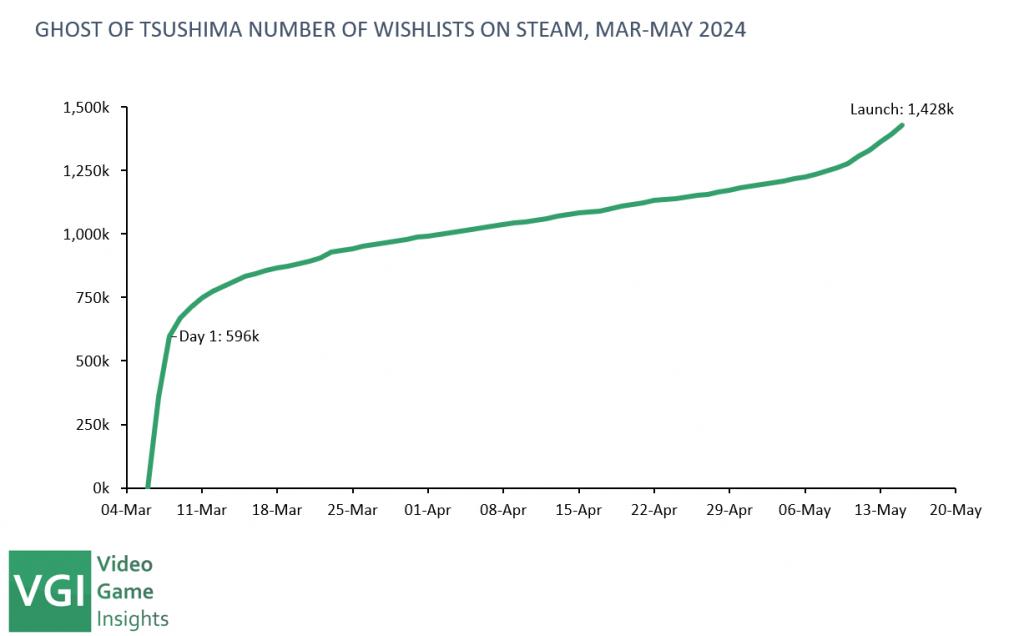

This success highlights the effectiveness of PlayStation’s Steam strategy. Ghost of Tsushima built up nearly 1.5 million wishlists within a couple of months before its launch, indicating growing trust and anticipation for PlayStation ports.

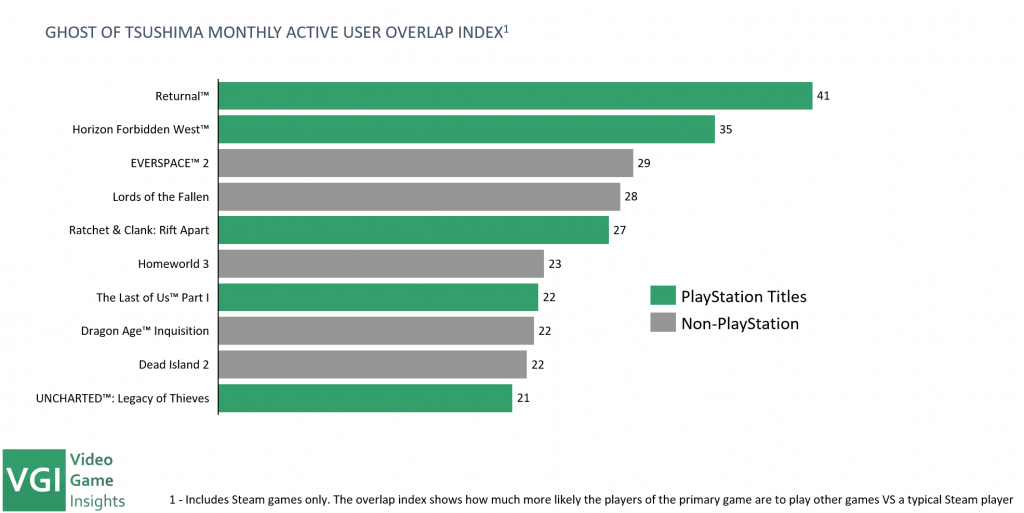

This can be seen quite clearly when looking at the Ghost of Tsushima player overlap

In fact, 5 of the 10 highest overlap indexed games for Ghost of Tsushima are PlayStation titles.

The Player Overlap Index shows how much more likely players of Ghost of Tsushima are to play other games VS your typical Steam player. You can read more about the Player Overlap Index here.

Has the move away from exclusivity and to PC paid off for PlayStation?

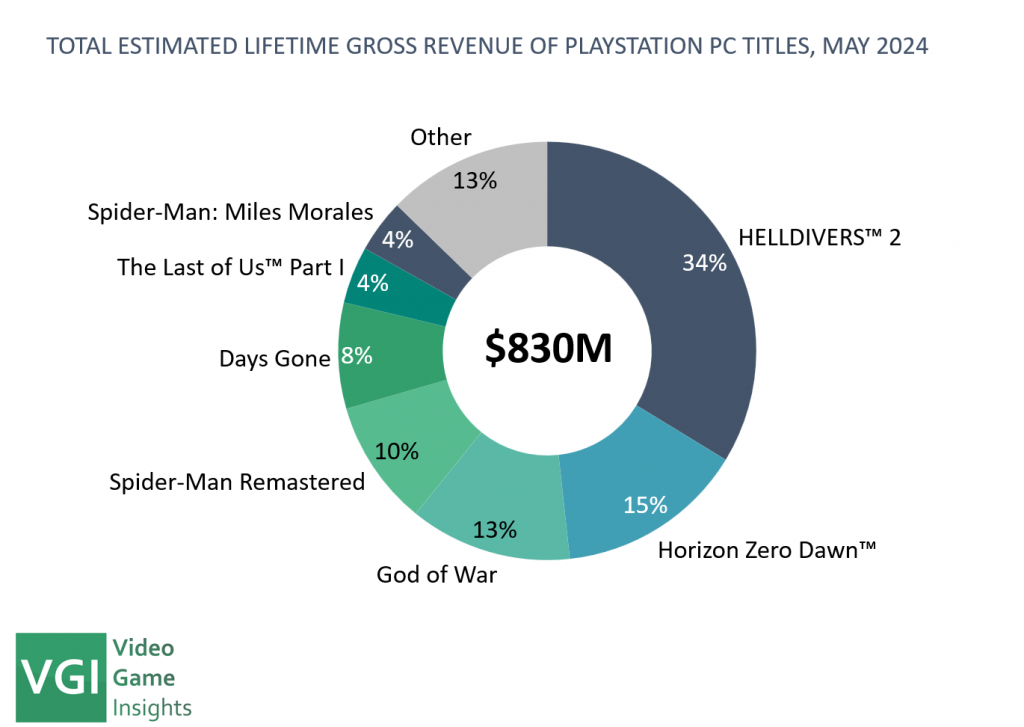

That’s a tricky question. It depends. PlayStation PC titles have generated an estimated $830 million over the last 4 years.

While impressive, this amount pales in comparison to the $29.4 billion generated by Sony’s Game & Network Services segment in FY23 alone. Of course, the G&NS revenue includes first party game sales, physical console sales, PlayStation + subscriptions, and importantly, the 30% cut they take from all sales on PlayStation Store. Still, it’s fair to say that the PC revenues on their own will never be a major segment for Sony’s gaming division.

For a fairer comparison, let’s examine PC sales relative to PlayStation platform sales using Horizon Zero Dawn as an example. Horizon Zero Dawn has sold about 24M units across PlayStation and PC by May 2023. 3.7M of that or c. 15% of total units sold were on PC. However, the PC pricing has been higher (even after Steam cut), given Horizon has been priced at $19.99 on PlayStation for the last 6 years.

We estimate that Horizon Zero Dawn has made approximately $120M on PC to date and around $500M on PlayStation. Therefore, releasing Horizon on PC has resulted in a roughly 25% revenue increase, a substantial boost for minimal effort.

With an estimated development budget of $47M (incredibly low for a AAA game of this quality) it means that the PC port alone has paid for the development of the entire game many times over.

Will PC players convert to PlayStation?

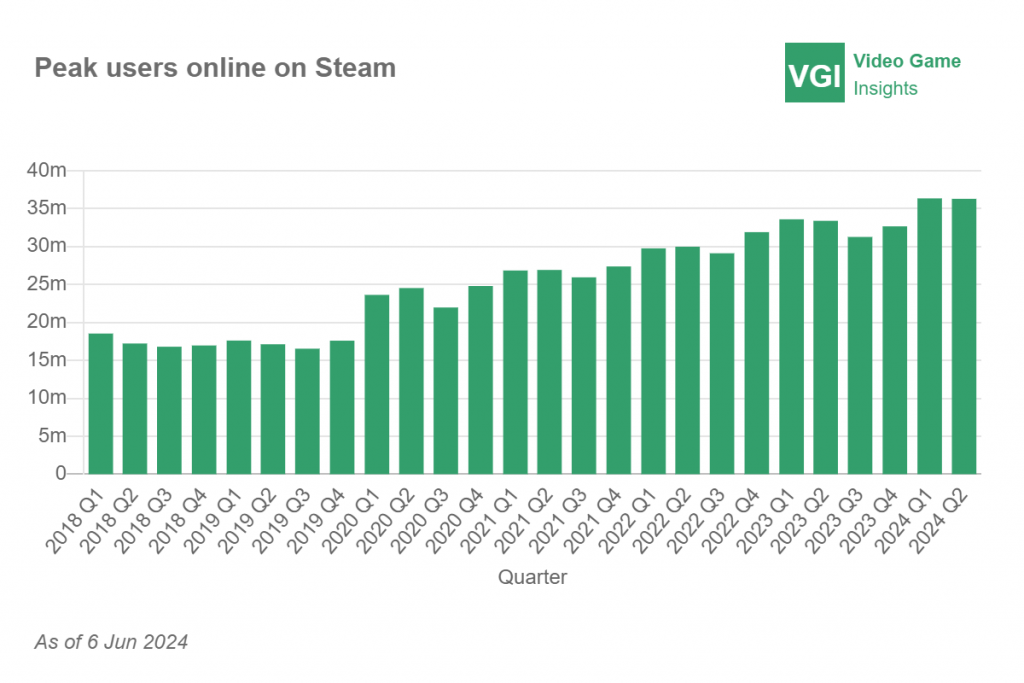

If Reddit is to be believed (and it almost never is), no PC player would ever betray their so-called “master race” and they would never do such an embarrassing thing as to move to PS5. And the truth is, there is a group of hard-core PC players who never will. But this group is getting proportionally smaller. Steam is not a niche platform anymore. There are now over 35 million people active on Steam at any given time, nearly double the pre-COVID numbers.

The majority of these players are not hard-core gamers and die-hard PC fans anymore. The casual and mid-core player mix is growing and that’s exactly the audience that Sony can attract. As the PC player base grows and diversifies, the “PC players don’t care for story-based single-player games” will hold less true. Having these games on PC can arguably also serve an “educational” purpose. How can you learn to love these experiences if you never get to try them?

Breaking down the walls of exclusivity

Other publishers have noticed PlayStation’s success and are announcing similar plans to adopt “multi-platform strategies.” Most recently, Square Enix revealed that they are “aggressively pursuing a multiplatform strategy.” While Xbox games have been available on PC for some time, they are now experimenting with bringing some titles to PlayStation.

In a period of slower industry growth, companies are breaking down barriers in search of new opportunities beyond their existing ecosystems. Gamers benefit from a broader access to high-quality titles, while publishers enjoy increased revenue streams and a larger, more engaged audience.

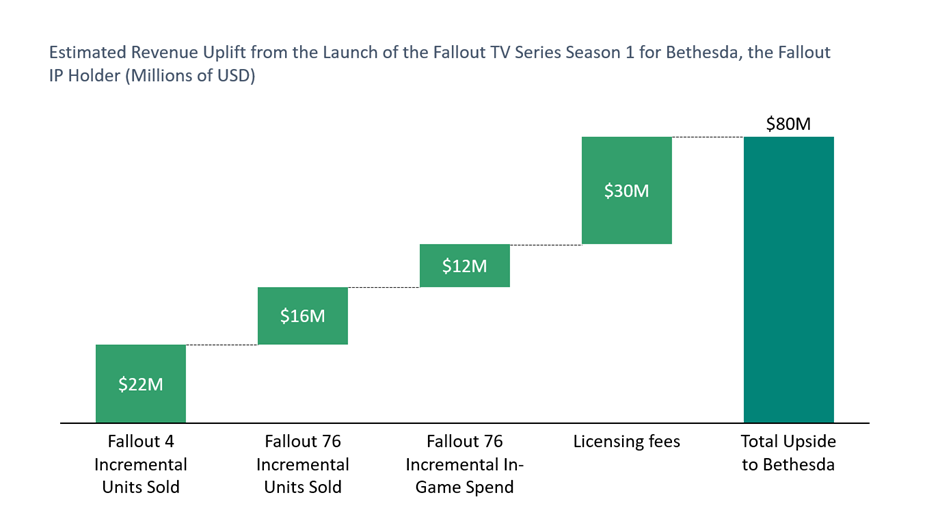

TLDR: The Fallout TV series made Bethesda an estimated 80 million dollars in game-related revenue and license fees with just one season. The TV show revitalised interest towards the franchise, boosting game sales and in-game spend. The potential lifetime value of this to Bethesda, the Fallout IP holder, is hundreds of millions of dollars.

Transmedia is a growing trend in the games industry, though it’s not a new concept. Companies like Disney have long used it, spreading their IP across films, TV shows, comics, toys, theme parks, and video games. Essentially, transmedia maximizes IP value by expanding into new platforms and formats, attracting new fans, and engaging existing ones.

Common types of transmedia involving video games

Book to Game

Some amazing games began as books. The Witcher series, starting as a book by a Polish author, found its first global audience through video games and then expanded further with a popular TV show. The Lord of the Rings and Harry Potter also started as books, moved to TV, and then became games.

Rationale: Some book worlds are so detailed that they can quite naturally be transitioned to games. From a commercial perspective, leveraging an existing fan base mitigates downside risk and there is upside potential to expanding the IP to new audiences.

TV to Game

Another successful example of franchise expansion has been existing TV franchises licensing the IP to video games. Disney has some of the earliest examples of that through Mickey Mouse, but also some of the more recent ones through licensing Marvel and Star Wars IPs.

Rationale: Creating games based on existing TV IPs is unlikely to reach many new audiences. However, it offers an attractive additional monetization mechanism for the IPs targeting younger audiences who are often gamers anyway.

Game to TV

Historically, expanding game IPs to TV has been less successful. Even five years ago, many believed it didn’t work because games are niche, with hardcore audiences, and their interactive nature is hard to translate to film. Examples of failed attempts include Max Payne, Warcraft, Gran Turismo, and Assassin’s Creed, which had potential but fell short commercially and critically.

However, the last 5 years has seen successful transmedia examples. The Last of Us was a masterpiece, loved by critics and audiences alike. Nintendo IPs like the Super Mario Bros Movie and Pokémon Detective Pikachu were commercial hits. Both Dota and League of Legends have released successful anime TV series. Most recently, the Fallout game franchise’s TV series on Amazon was a major success and positively impacted the games.

Rationale: A successful TV show can re-engage existing players (useful for live service games) and expand the market of interested people, offering significant upside for the IP holder by boosting player engagement and attracting new audiences.

The Success of the Fallout TV Series

Firstly, it is important to understand that Bethesda, the game’s IP owner and Amazon, the producer and TV streaming platform owner, are two separate entities that benefit from this TV show in very different ways.

Impact of the Fallout TV series to Amazon

The impact on Amazon is clearer and easier to capitalize on. TV streaming services release content to attract new audiences and retain existing ones. While retaining viewers often means providing a lot of content, attracting new audiences requires big hits like the Fallout TV series.

Here’s what we know about the Fallout TV show viewership:

65M viewers in the first 2 weeks – The Fallout TV show is Amazon’s second most-watched TV show ever, only behind The Lord of the Rings: The Rings of Power.

Mostly watched by 18-34 year olds – Important as Amazon aims to reach new, younger audiences.

60% of the audience from outside of US – Beneficial for expanding Amazon’s primarily US-heavy audience.

It’s clearly been successful for Amazon, even if we can’t put exact revenue or profit numbers to it. What about Bethesda, the IP owner?

Impact of the Fallout TV series to Bethesda

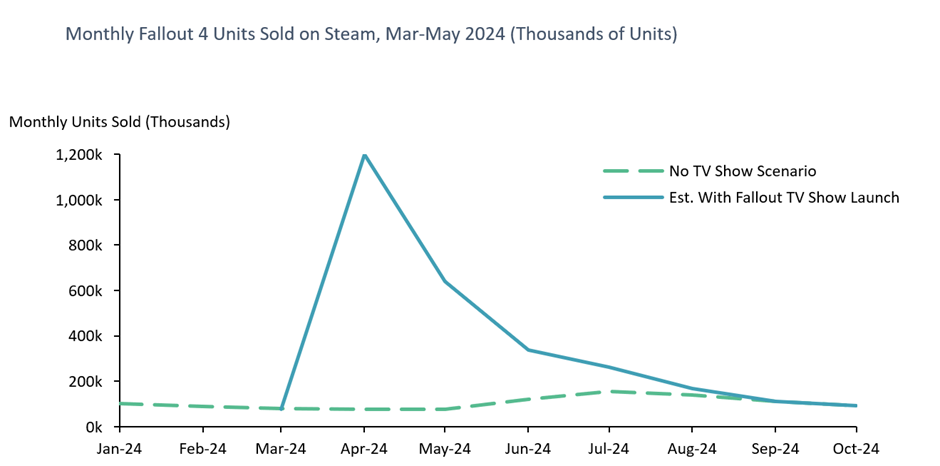

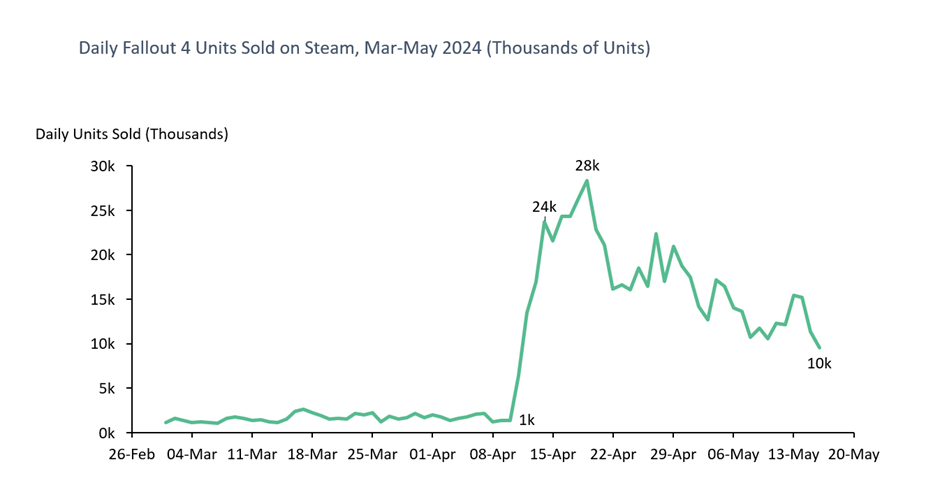

Methodology – Each of the revenue opportunities for Bethesda is calculated by analysing the uplift in Fallout game metrics at the time of the TV show’s launch and forecasting the trend forward to September, when we estimate most of the upside has been realized. We have only considered the impact to Fallout 4 and Fallout 76 here. We don’t cover Fallout Shelter as we lack the data behind it, so we’re likely underestimating the total impact by c. $5-10M. There is additional upside from other games, but at much lower magnitudes. The metrics are estimated using data from the Video Game Insights platform. For Fallout 4 units sold, it looks like this:

Cost – Bethesda likely incurred very little expense, as Amazon probably covered most of the marketing, production, and distribution costs. This means the revenue uplift for Bethesda is almost pure upside.

There are four main revenue uplifts to consider:

Increased game sales – Renewed interest in the franchise boosted sales of existing games.

More in-game revenue – Increased active players for live service games, including both new players and reengaged former players.

Licensing fees – Bethesda was likely paid substantial fees for the right to use the IP.

Expanded audience base – A larger audience base for future game releases.

Here’s what we think the value of each of these buckets looks like:

Increased game sales – We estimate that the TV show will generate an incremental c. 2M Fallout 4 game units sold and c. 1-1.5M Fallout 76 units. That’s roughly $35-40M in revenues post platform fees (taking promotional discounts into account).

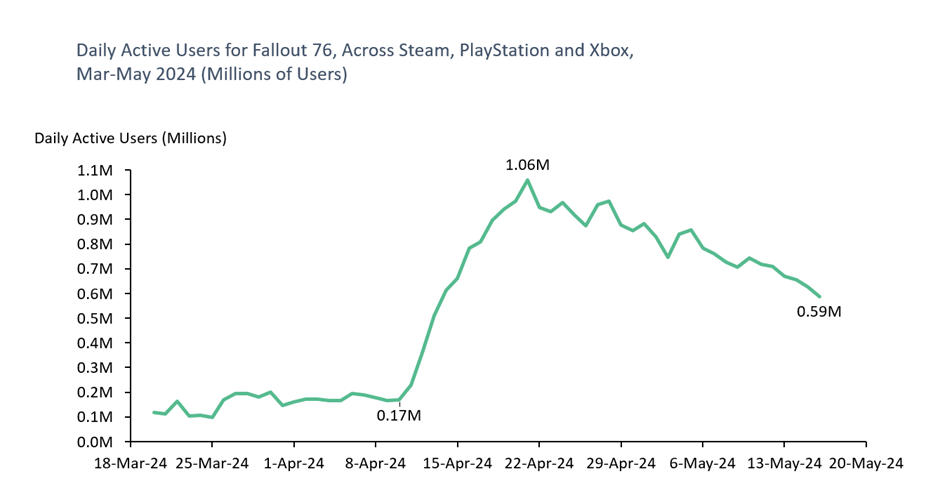

Higher in-game spend in Fallout 76 – Daily active users of FO76 increased from c. 100-200k pre show to peaking at 1M DAU during the show’s launch window across all game’s platforms. This will likely slightly dilute the average revenue per daily active used (ARPDAU) as the new players tend to be more casual. We estimate the increased engagement from old and new players to deliver c. $10-15M in incremental in-game revenues for FO76.

Licensing fees – It is very hard to put a price to that without knowing the details, but typical game and physical goods IP license fees tend to be c. 10-20% of the revenue generated. We also know that Amazon bought the global rights of the Lord of the Rings for $250M or c. 25% of the 1st Season’s budget. Given the $150M budget for the Fallout TV show, it’s not unreasonable to assume c. 20% of the budget was on IP licensing. That would give Bethesda a c. $30M licensing fee.

Overall, the total value from Season 1 of the show that Bethesda will get is likely c. $80 million.

Is $80 million good?

You might think this is a stupid question. However, we’re talking about Bethesda (acquired for $7.5bn), a company that is owned by Microsoft ($200bn annual revenue). In this scale, $80M means a 0.05% uplift to Microsoft revenues, which is ridiculous to think about.

Perhaps that’s not the right comparison though. Let’s compare this to a major AAA game launch like Fallout 4. Fallout 4 sold over $750M worth of games in its first day and we estimate the lifetime earnings have been closer to $1.5bn across all platforms. That’s not atypical for a major AAA title. In this context, the Season 1 revenue uplift of c. $80M to Bethesda is c. 5% of total game sales, still relatively small.

However, this analysis doesn’t consider several factors.

Firstly, we’re only assessing the impact of Season 1. Fallout TV series has already announced Season 2 and it’s likely there will be more to come. So, the impact can be many times that.

Secondly, the series brings a much bigger total addressable audience for future Fallout games. The jury is still out on the actual financial impact of this. However, we bet that Fallout 5 (or 6 or whatever we’ll call it) is going to be planned around one of the Fallout TV show seasons launches.

We estimate that the full value of the Fallout TV series to Bethesda is in hundreds of millions in extra revenue. Importantly, this is a very low risk, low-cost revenue uplift opportunity.

Importance of a well-planned content schedule post TV launch

Bethesda did support the TV show launch with a new patch on PC, Xbox and PlayStation versions of Fallout 4. However, as far as new content goes, it’s really quite little. You could have imagined Bethesda aligning the TV show launch with a major downloadable content (DLC) or, better yet, a new game launch. Fallout 4, the last major single player title in the franchise is almost 10 years old, after all. No doubt they will be doing more to align content with next seasons now that they’ve seen the positive reception.

Transmedia – another buzzword or a real opportunity?

Hater’s gonna hate and hypers gonna hype. Cross-media opportunities provide a low-risk way for game IP holders to boost revenue, though the upside seems capped even in the most successful cases.

We predict many game IPs will be adapted for film and TV in the coming years. With slower growth in the games industry, executive teams will find these opportunities too attractive to ignore.

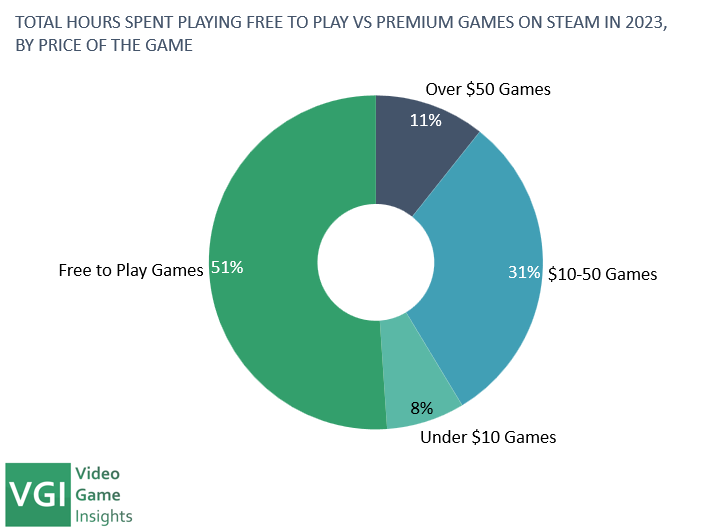

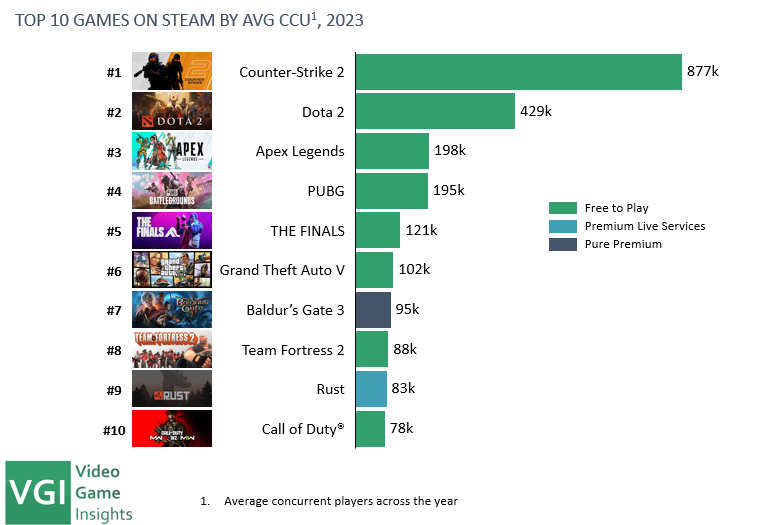

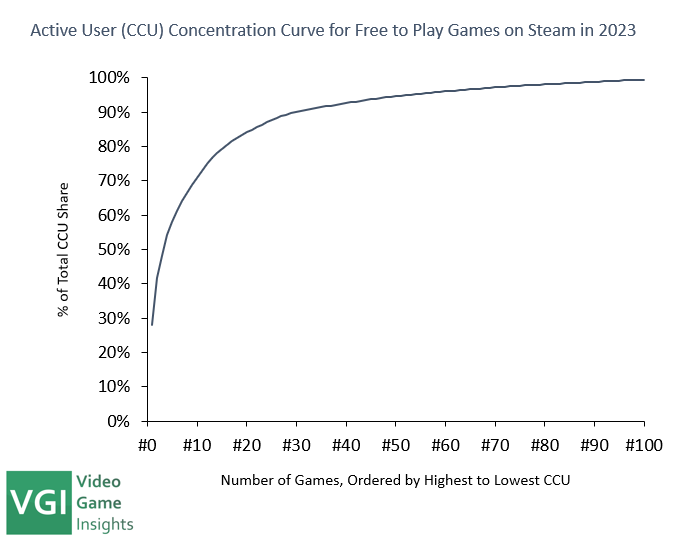

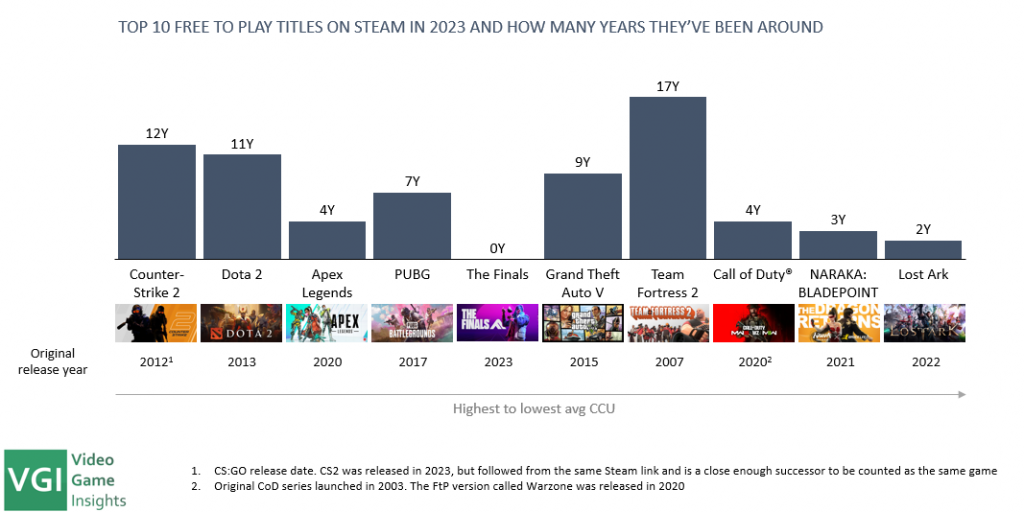

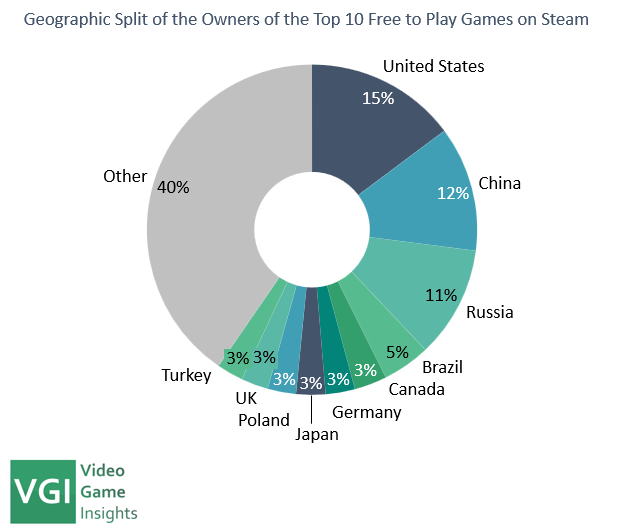

Free to play (FtP) has been a standard in the mobile games industry for over a decade now. In the PC and console world it became a bigger topic around 2017-18 when Fortnite took the world by storm. Suddenly, every large publisher needed to have their own FtP title.

But free to play really started at a meaningful level much earlier, on PC. There are the classics outside of Steam – Runescape (2001), Wolfenstein: Enemy Territory (2003), Silkroad Online (2007) as well as examples on Steam – Team Fortress 2 (2007), DOTA 2 (2013) and so on.

Which brings us to the state of free to play games on Steam in 2024. This report explores the popularity of FtP within Steam and looks at the top games over time.

You’re not going to believe trend number 4! (just baiting you to read the report)

Video Game Insights provides free articles and market reports as well as a comprehensive data and intelligence platform for developers, publishers and investors. Use the menu on the left to explore our tools or search for any game or games company in the search bar above to get started now.

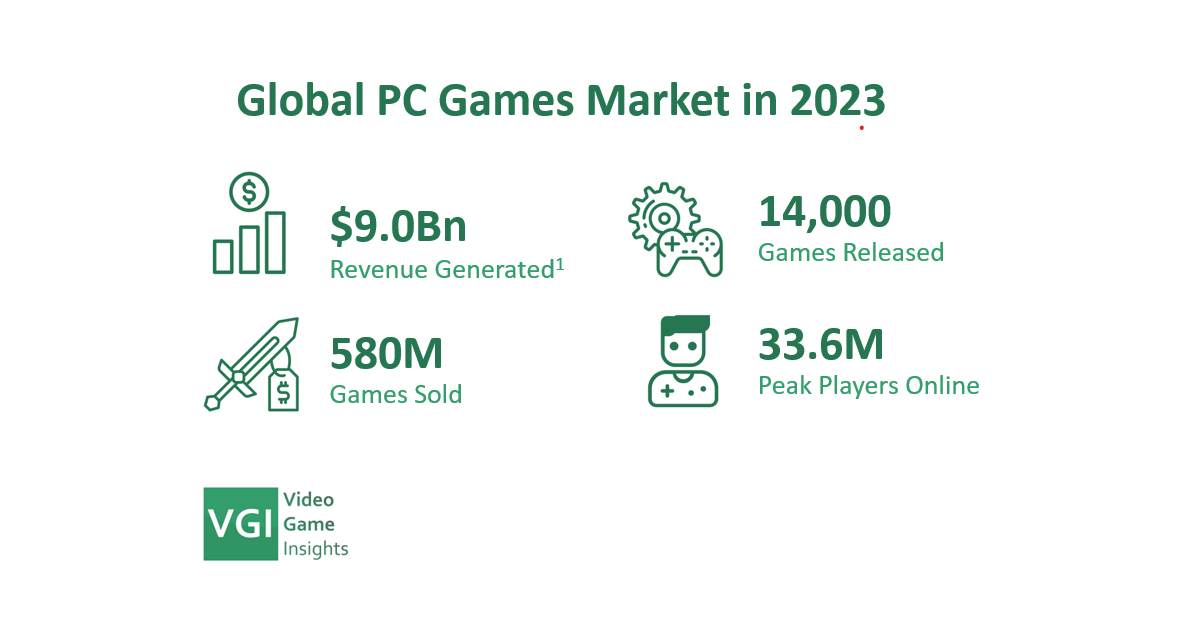

Wondering how the PC gaming market managed to achieve its highest ever revenues in 2023? Our global pc market report 2024 unveils the driving forces behind the growth as well as industry trends that will guide the market in the next 5 years.

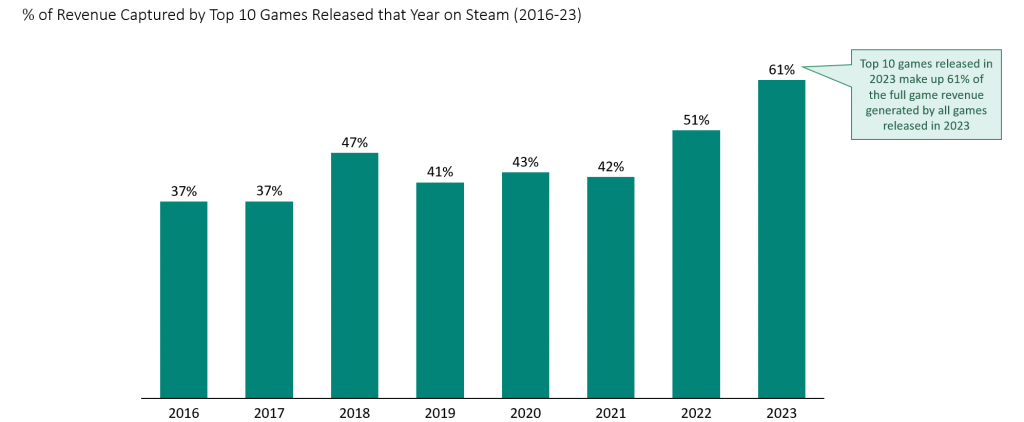

The PC market set records in 2023 with highest ever revenues, units sold, peak players online and number of games released on Steam.

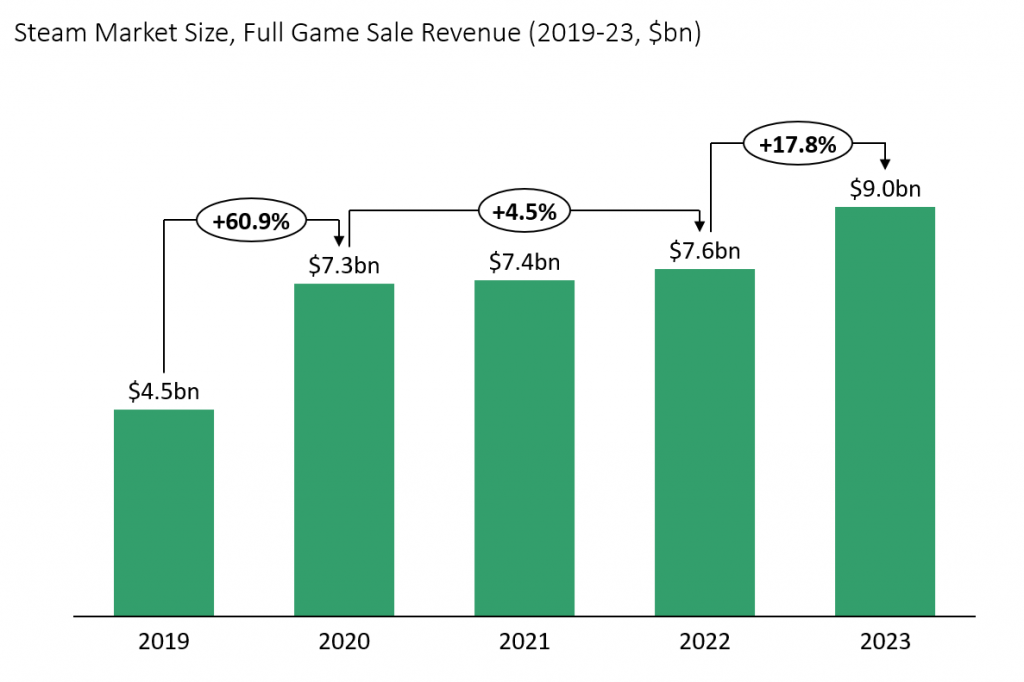

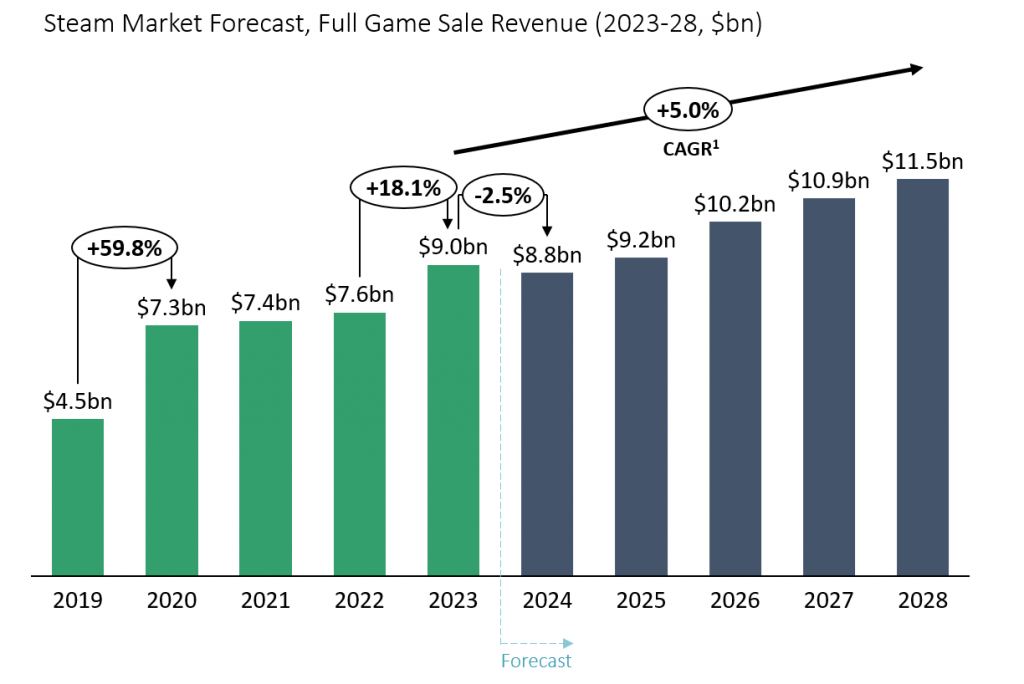

2023 saw over $9bn gross full game revenue generated on Steam with 580 million game copies sold and about 14,000 new games released.

Total gross revenue from game sales (excluding microtransactions) grew by 17.8% in 2023. This comes after several years of flat revenues as the games industry was recovering from the COVID boom.

PC games market will continue to grow at approximately 5% per year for the foreseeable future. However, 2024 is expected to be a down year. A weaker slate of new releases, combined with an exceptional 2023, makes it challenging to forecast growth for 2024, despite some positive tailwinds.

The PC games industry has become increasingly “winner takes it all” over the last 8 years. Top 10 releases of 2023 made up 61% of the total revenue generated by new releases.

Steam covers vast majority of the PC market these days and the trends on Steam are broadly reflective of other, much smaller PC games stores. Therefore, our report is largely based on Steam data.

Video Game Insights is not affiliated with Steam or Valve and all data provided is estimates.

Explore our platform to learn more

Video Game Insights is powering the creativity in the games industry through data. We provide free articles and market reports as well as a comprehensive data and intelligence platform for developers, publishers and investors. Use the menu on the left to explore our tools or search for any game or games company in the search bar above.

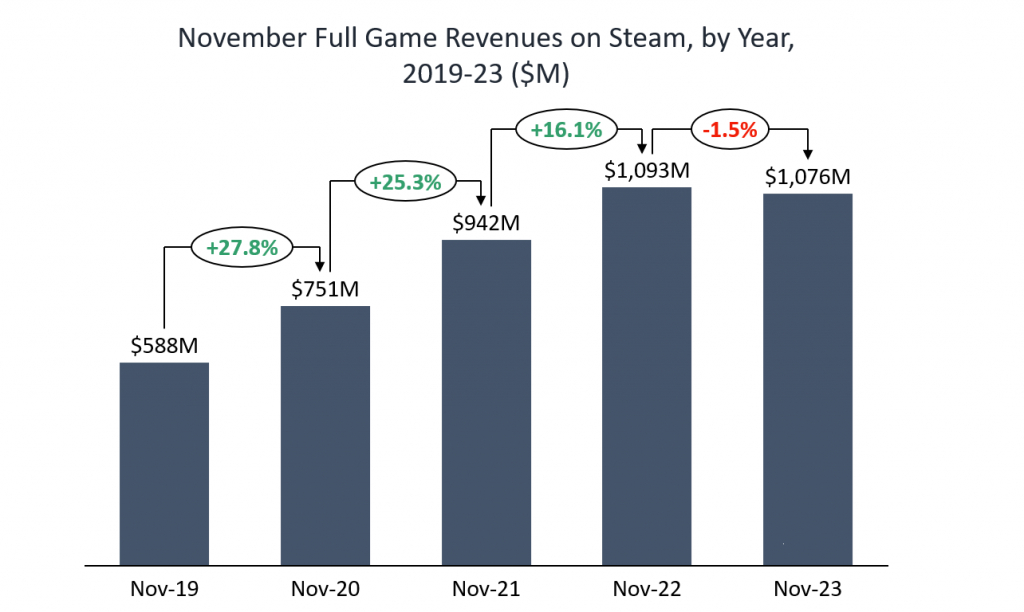

Steam has been hitting records across many metrics as we’re entering the holiday period. Full Game revenue for 2023 has already beat last year’s and we’ve still got a busy month ahead.

Black Friday performance is no exception. A year of strong game releases tied to unprecedented attractive promo deals has pushed 2023 Black Friday to highest units sold ever.

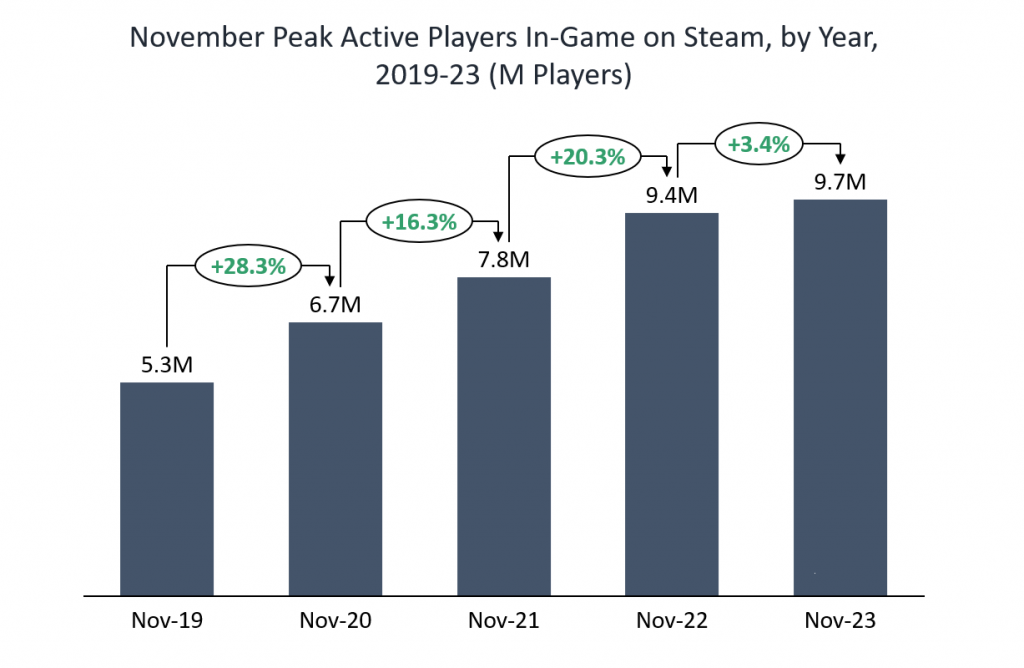

User engagement keeps breaking records on Steam despite the post-covid normalization

Covid helped to boost the whole games industry with people stuck inside and nothing better to do. New people picked up gaming as a hobby and old gamers had more time to game. The post-covid world has been tough for the games industry – years of growth that culminated with a peak in 2020 have turned to stagnation and even decline.

The exception to this has been the PC gaming space where Steam has continued to hit new record levels of engagement. Peak active users have continued to push past the Covid peak of April 2020.

The Black Fridays are no exception – 2023 November saw another record in terms of peak active players in-game on Steam.

However, this growth in engagement has clearly slowed. In fact, 2023 November peak was only 3.4% higher than last year’s.

At least partly, availability of the next generation of consoles can be blamed for this slowdown. It’s been 3 years since PlayStation 5 and Xbox X were released, but it wasn’t till 2023 that the supply really started to catch up with the demand. People who had to substitute their preferred console for PC are now able to return to… well, let’s be serious – to PlayStation.

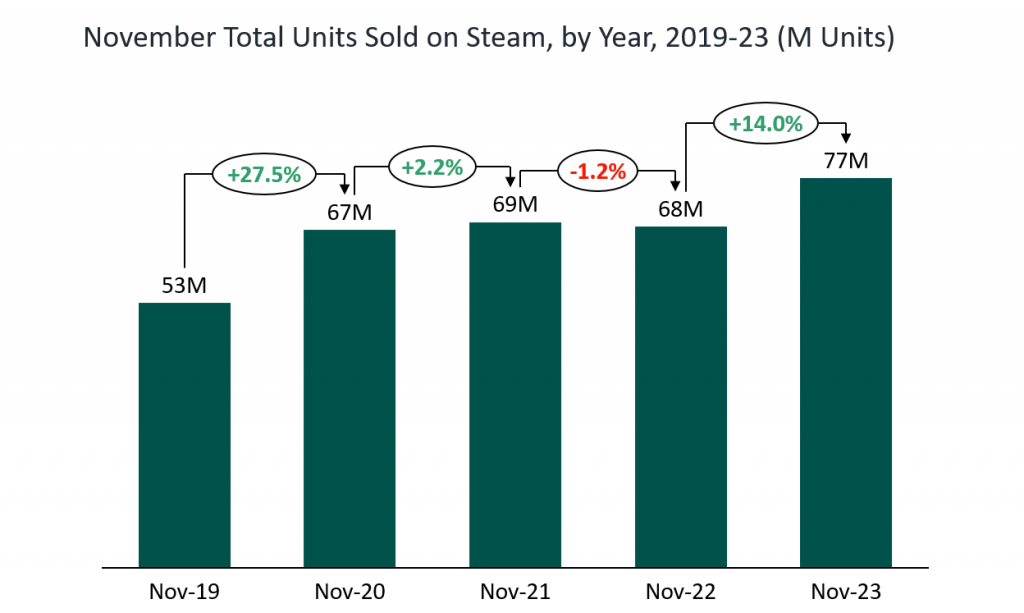

2023 is a year of significant growth after the stagnating Black Friday sales on Steam in 2021-22

Even though engagement continued strong on Steam, units sold have stagnated since 2020. Players had a large library of existing games to play and new releases were underwhelming or delayed.

2023 broke that with a strong release slate. While some of these anticipated releases underperformed expectations (Starfield, anyone?), others beat even the wildest of predictions (Baldur’s Gate 3).

This has resulted in the strongest ever Black Friday sales on Steam, beating 2022 by 14%.

Deeper discounts were the first tool to be used by publishers in the fight for limited attention

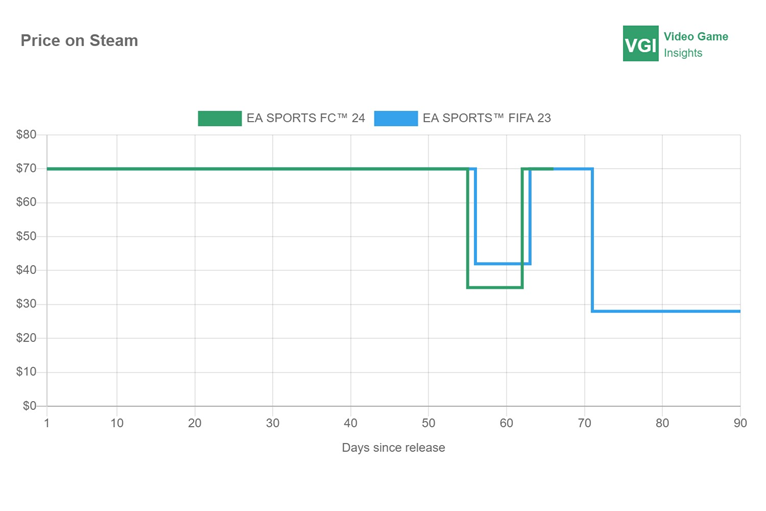

2023 has been a tough year for many publishers as the market is getting increasingly saturated and new player growth has slowed. A natural response to that has been discounting more to boost visibility and discoverability.

EA Sports FC was on 50% sale across all platforms less than 2 months after release – the steepest ever promo for them.

Other big name 2023 releases have also gone as far as 40% off less than a year since release. Although not atypical for large titles, the amount of discounted big releases still played a role during the Black Friday.

Slightly declining Black Friday revenue is a sign of fiercer competition among publishers for an increasingly fixed size of the pie

Higher engagement and record units sold failed to translate into higher revenues during Black Friday.

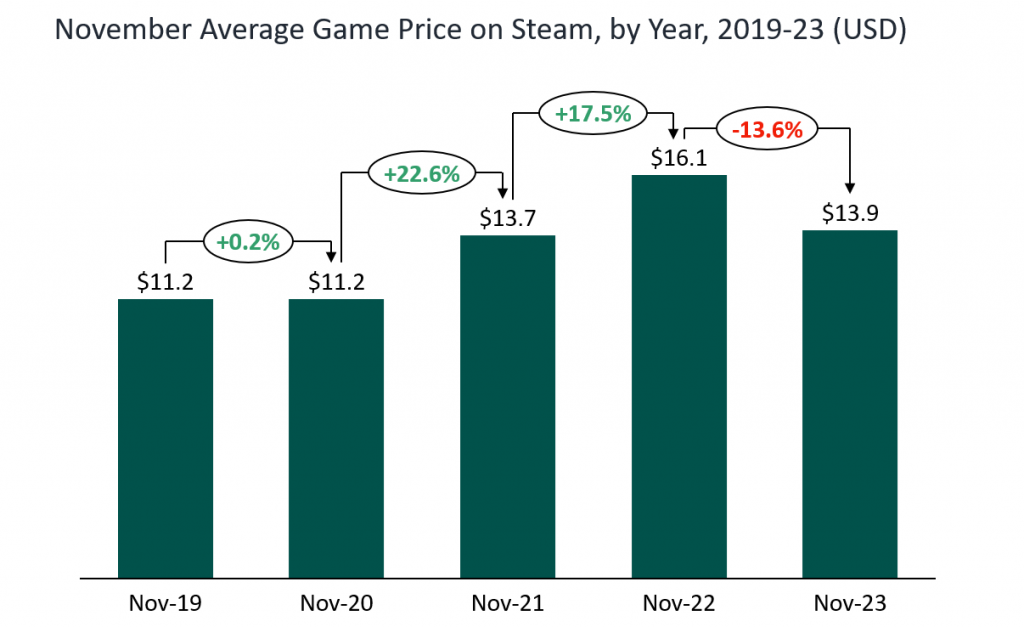

In fact, while units were up +14% YoY, full game revenue was down -1.5%. This was largely driven by steeper than usual discounts boosting units, but at lower average selling price. Players’ overall lower disposable income this year and higher competition between games due to strong releases has led to a push to the bottom as publishers are fighting for attention

Price pressure likely to continue as the games industry is facing increased supply and peaking demand

The decline in average game selling price is likely to continue as several games industry dynamics push the prices to the same direction:

Subscription platforms such as Xbox Game Pass are likely to continue to offer great value for money in the coming years with many day 1 releases appearing free on the platforms

Economic downturn is affecting consumers’ disposable income, leading to a decrease in spending on non-essential items, including video games. Publishers are already responding by offering more discounts to maintain sales volume

Slowdown in gamer growth is a global trend as Covid pulled many gamers to be forward. The markets that continue to grow tend to be more price sensitive. The new users that aren’t already gamers tend to be more casual, also pushing down spend

Increased competition between publishers on the ultra-premium games side. Many AAA publishers have adapted the same strategy of fewer, but higher quality games released

Lower costs on indie studios through easy-to-use game engines like Unreal Engine 5 and AI support in asset creation helps small teams to create increasingly complex games, increasing the overall supply of good quality games

Longer and more replayable games have been a trend for many years now. However, the evergreen nature of some of these games is creating a dynamic not seen in the games industry before where new releases compete for attention with games that are over 10 years old

The pressure to discount sooner and deeper will be good for gamers in the short term. However, the increased pressure on studio margins will likely result in more redundancies, streamlining and efficiency, which ultimately might not be the right formula for best games.