We’re excited to announce that we are now part of the Sensor Tower family. This acquisition will allow us to significantly boost our platform offering and the speed at which we can deliver new features to our clients. Our combined gaming intelligence solutions will include PC, Console and mobile insights, providing customers with an unparalleled view of the gaming landscape.

🚀 Video Game Insights will now operate as “Video Game Insights by Sensor Tower.” 🎮 Click here to read the full announcement

We will release a lot more information about our future plans in the following weeks. Stay tuned!

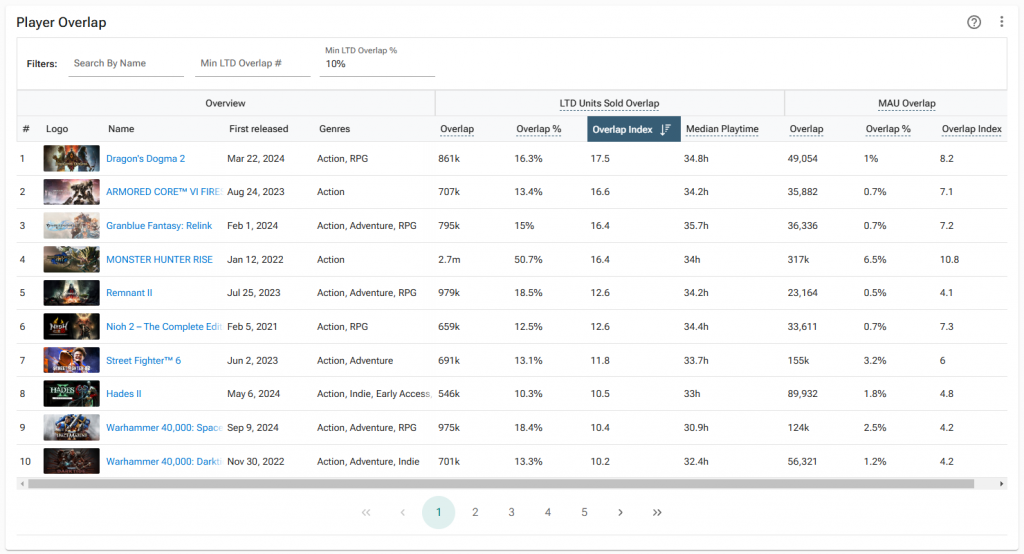

This update comes with a bunch of smaller bug fixes and visual updates. However, the bigger new feature allows you to now filter the Player Overlap tool in a better way.

You can now easily combine the power of overlap % and overlap Index. For example, you could only look at games with at least 10% overlap and sort by overlap index. This would result in only larger games being shown, but still ordering by their relative persona preference.

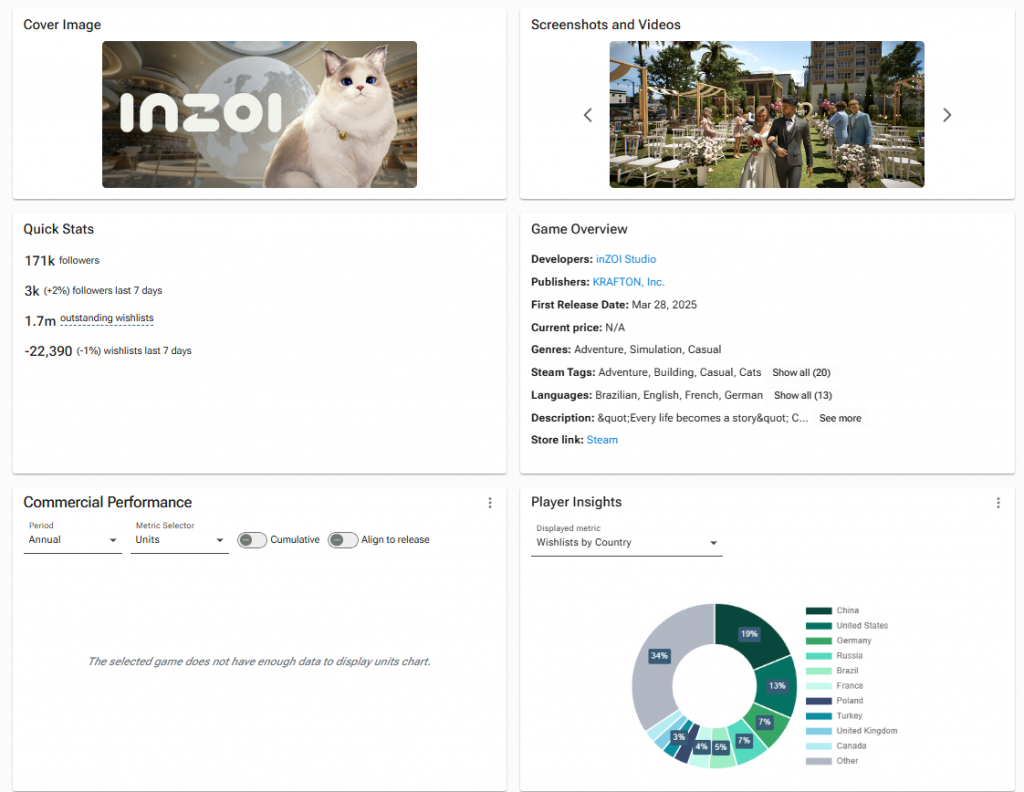

We are now showing wishlist breakdown by country estimate for unreleased (and also released) games! You can now see where the interest towards a game is coming from.

We have added a couple of much requested features to the paltform recently:

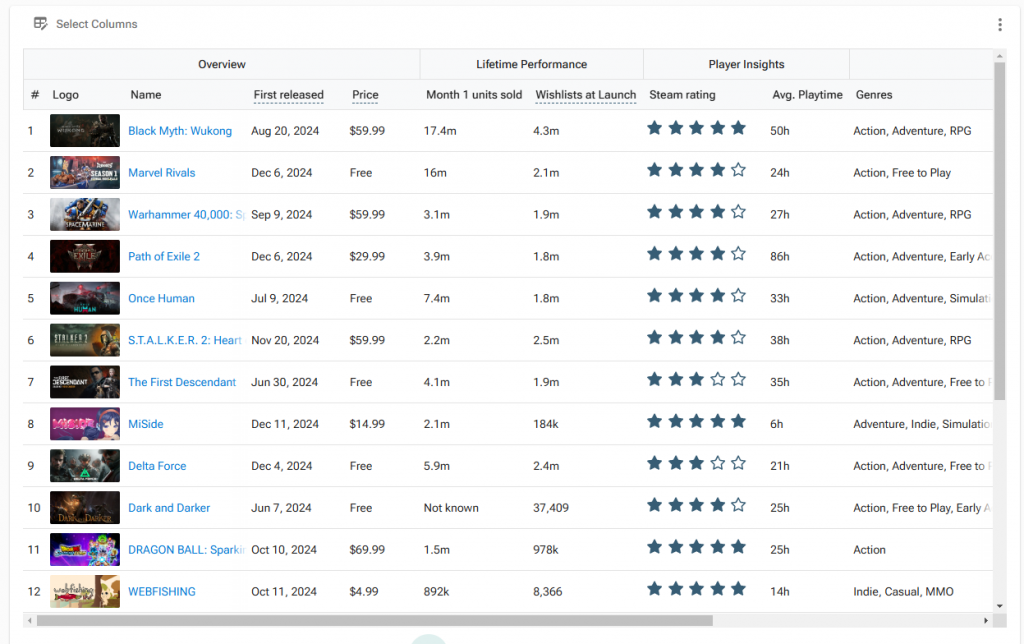

Month 1 and Year 1 units sold on Games Database

We’ve added 2 new columns to the Games Database – Month 1 and Year 1 unit sales. This allows you to have quick like-for-like comparison for launch performances.

Not only that, you can use these together with our “wishlists at launch” metric to get a better understanding of the wishlist to launch conversion ratios for the games you care about.

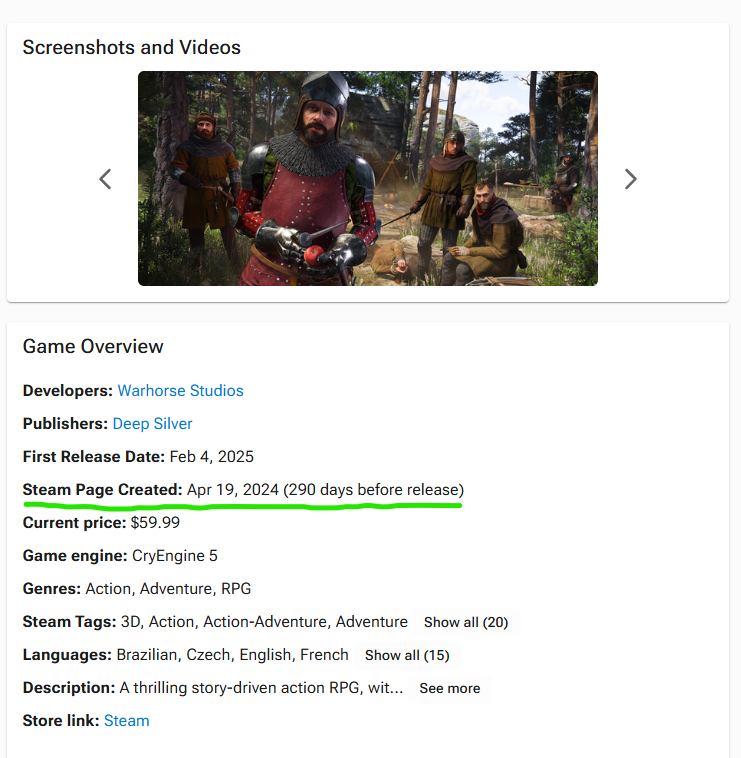

You will be now able to see when the actual Steam Store page was created for majority of games, including how long it took them to get from Store page creation to launch.

This is a super useful metric for understanding how to optimize the Steam page and how early other games release their Steam pages pre launch.

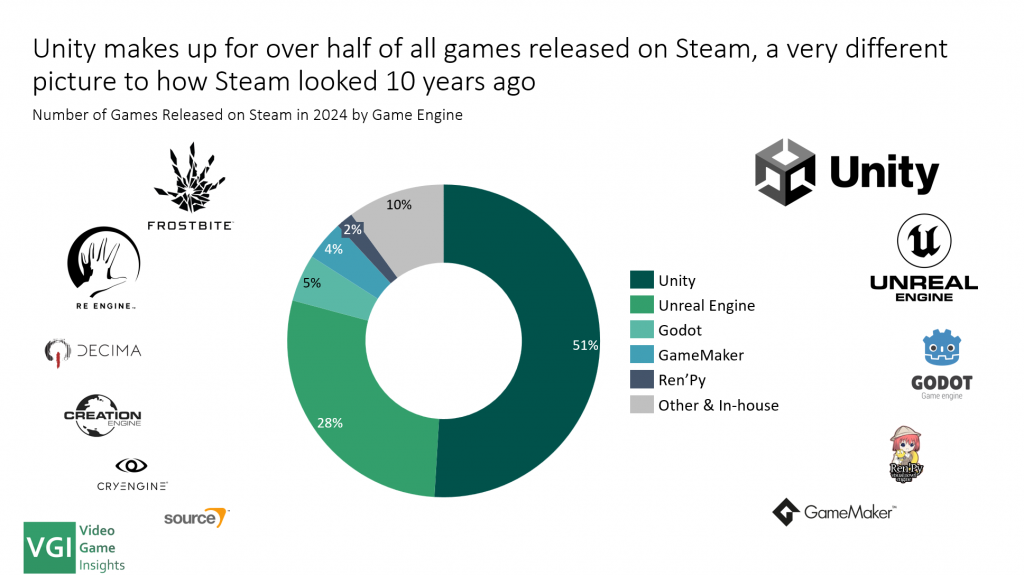

Video game engines have evolved significantly over the past decade. While mobile game development has long been dominated by third-party engines—most notably Unity—the same was not true for PC and console games.

Until recently, the majority of large titles were developed using in-house, custom-built engines. Not anymore.

This report covers:

– State of game engines today – Game engine market share trends over time – Forecasting the future trends – Did Unity’s pricing debacle impact market share? – The growth of Unreal Engine – Is Godot really winning share? – Game engine shares by sub-genre of games

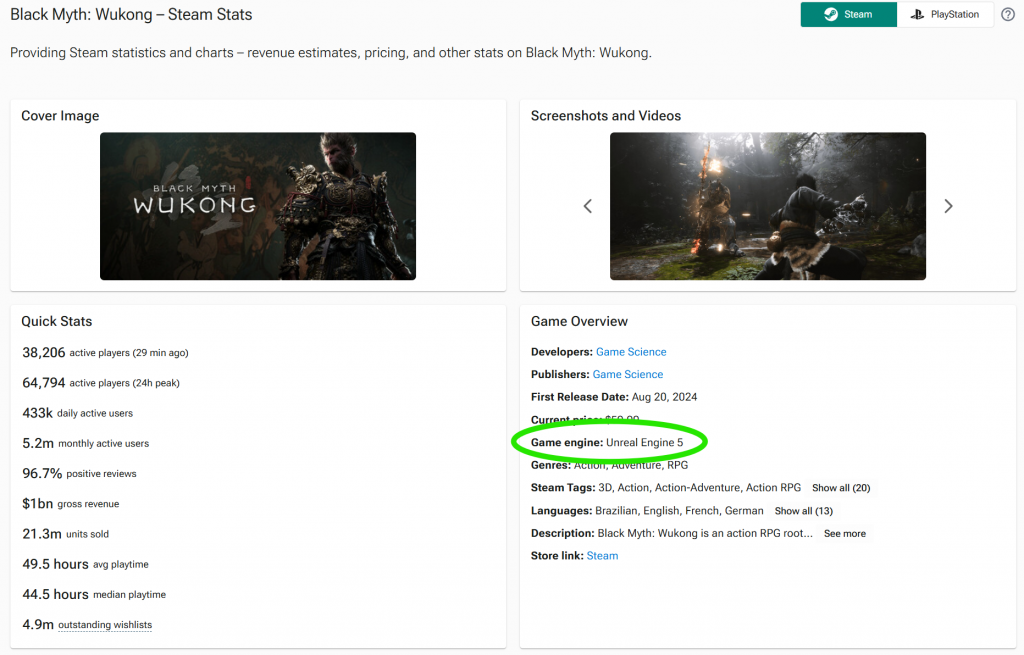

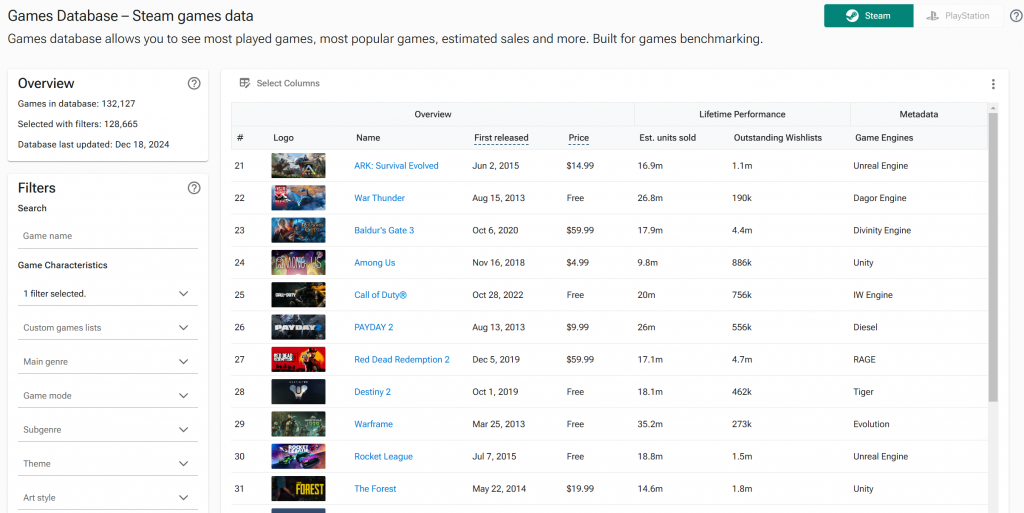

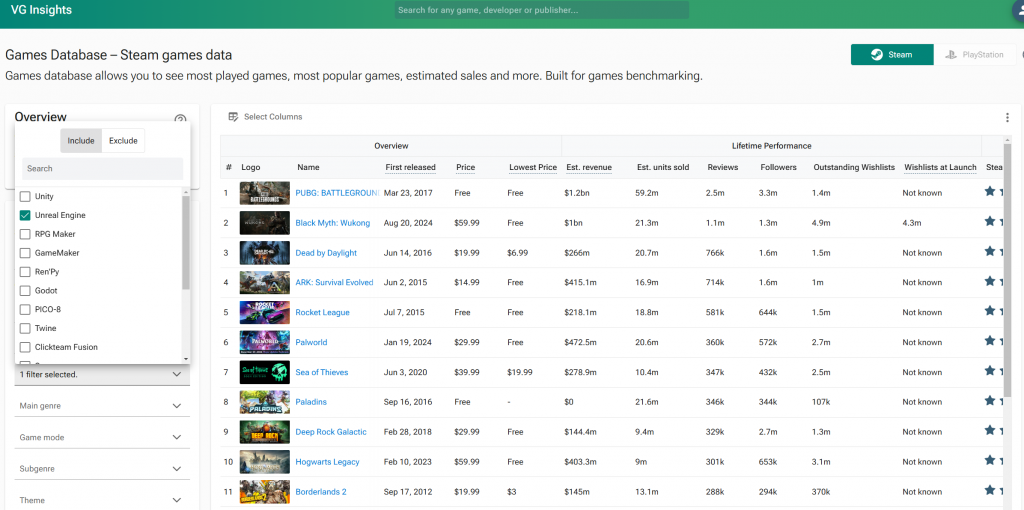

We have just added game engines as a datapoint to all games. As a business subscriber, you’ll be able to see the game engines for most games with >10k sales.

Business subscribers will also be able to see game engines as a separate column in the Games Database.

You’ll also be able to filter games based on the engines!

Our wishlist estimates have been the best in class since we launched them back in March. Well, they’ve just got a bit better. We have had to tweak our methodology slightly and this has resulted in even smaller variance VS actual numbers in our internal checks.

Key changes:

Some games weren’t tracking wishlists properly before and they are now

Some games’ wishlists were overestimated before where we’ve now fixed that bias

This impacts all wishlist numbers we show. We encourage you to update any analysis that relied on the old numbers.

Note that we try and keep any large scale estimation changes to a minimum, but in order to provide you with the best estimates possible, we do occasionally need to make these changes.

We will make sure to give a heads up in the future rather than report any changes retroactively.

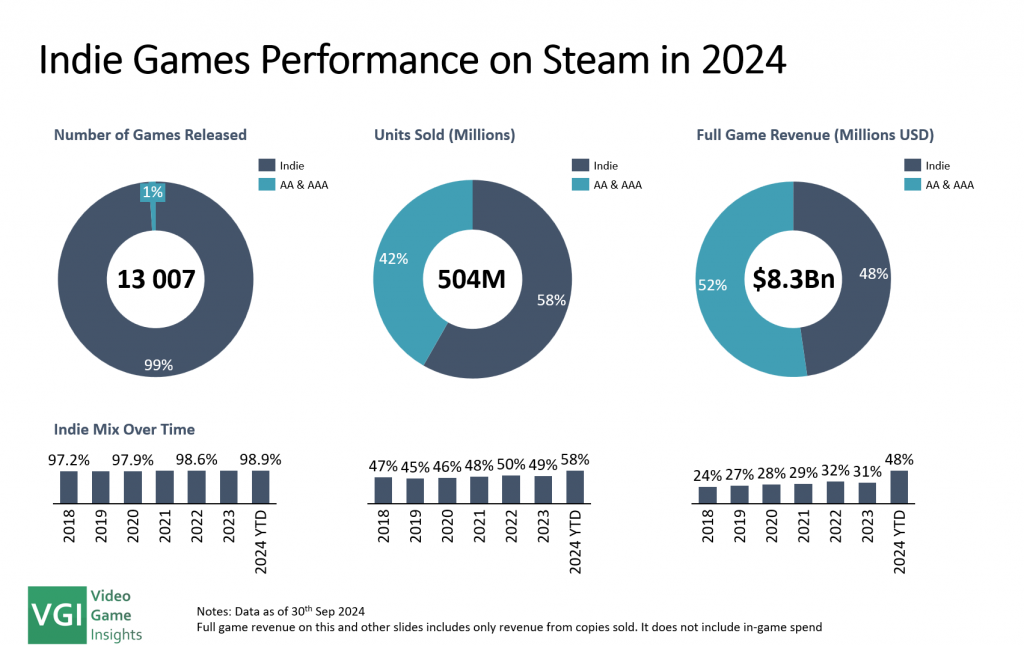

The global indie games market has hit new heights in 2024. Our Global Indie Games Market Report 2024 offers an in-depth analysis of the indie game landscape. Discover key data on market growth, top-performing games, and trends shaping the future of indie gaming.

Indie Games Now Rival AAA Titles on Steam: For the first time ever, indie games are generating as much revenue as AAA and AA titles on Steam.

Top Indie Game Releases of 2024: Black Myth: Wukong and Palworld have set new records, with tens of millions of units sold.

Growth of the Indie Market: Indie games sector has grown every year since 2020 despite the wider industry slowdown.

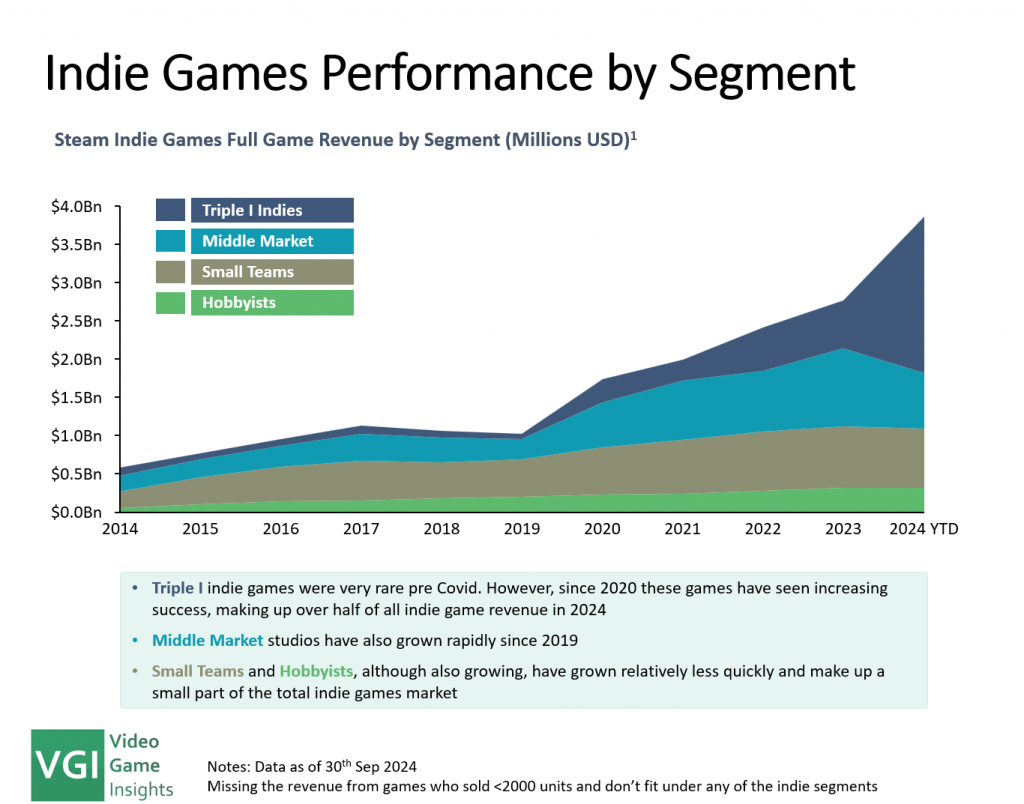

Segmenting the Indie Market: Indie market splits into Triple I Indies, Middle Market, Small Teams, and Hobbyists. Each segment has seen unique trends in the last 4 years.

Indie Studios are Maturing: More studios are releasing their 2nd or 3rd games, with experienced developers seeing better financial success with each release.

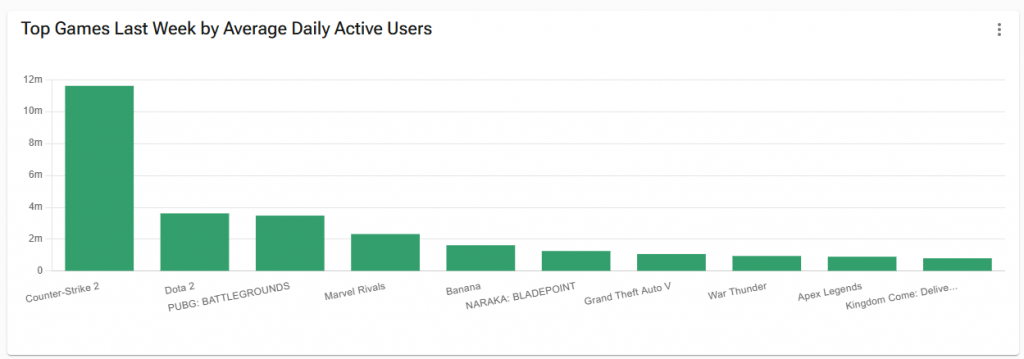

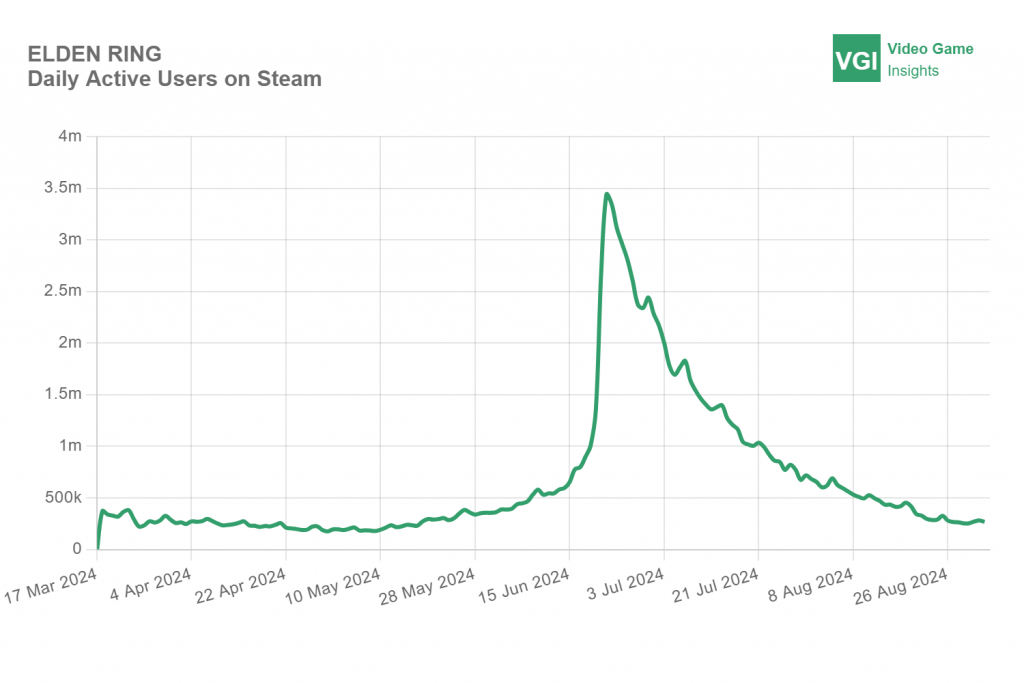

We’ve just released our estimates for daily active users (DAU) and weekly active users (WAU) for Steam games.

You’ll be able to see these metrics for any game with at least 100k units sold by going on their individual games page and using the “historical data” section.

Note that these metrics do tend to give a highly correlated view to the much used concurrent users (CCU) metric on Steam. However, DAU and WAU are much more used in corporate environments and serve as a more practical input for most modelling purposes.

Additionally, the DAU metric sets us up for the upcoming PlayStation data where you will be able to start comparing PC & PS DAU metrics and see what the platform mix looks like for multi-platform games.

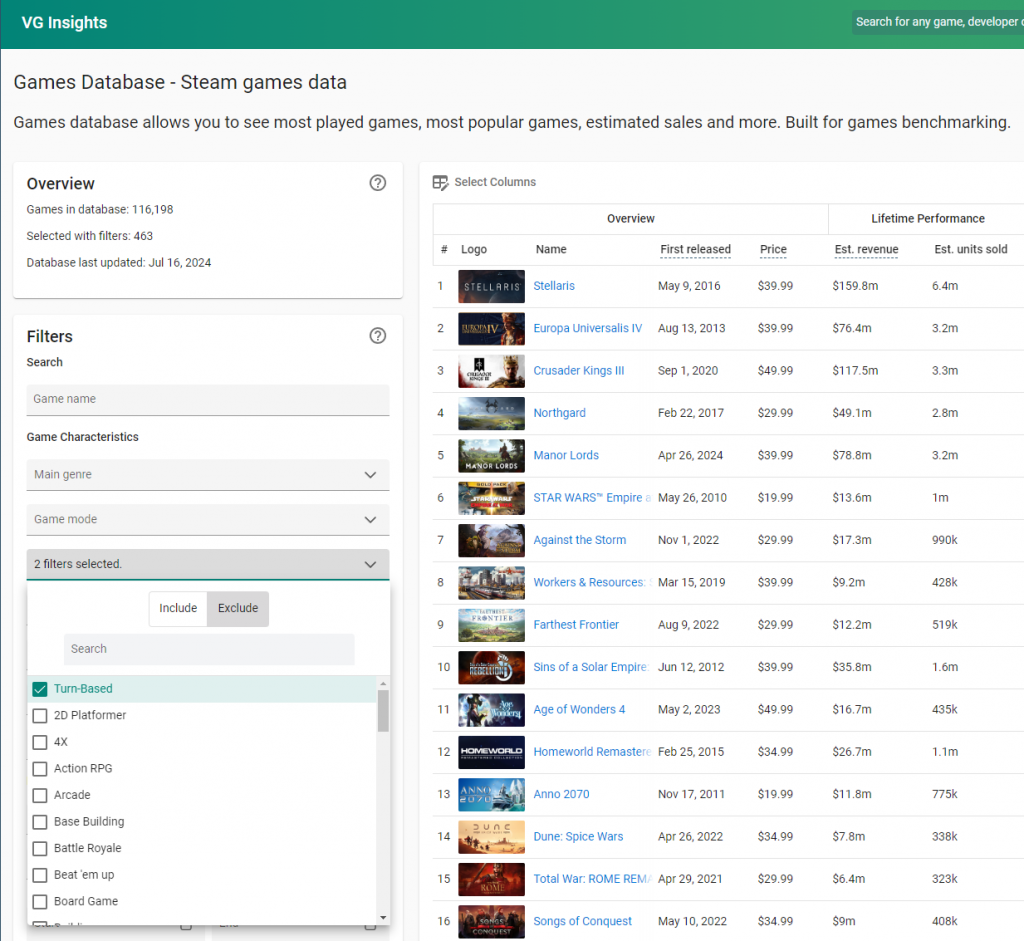

We have revamped our filter system, making it easier to use and improving its functionality.

Filters are available on many pages, from Steam Analytics to Games Database and can help you narrow down a list of games or companies to look at. We’ve long had an extensive list of filters to choose from, but we’ve now made it even more powerful to use.

Include / Exclude Filters

You can now include as well as exclude characteristics in filters. For example, you might want to see all 4x games, but exclude any turn-based games, leaving only real time 4x games in the list.

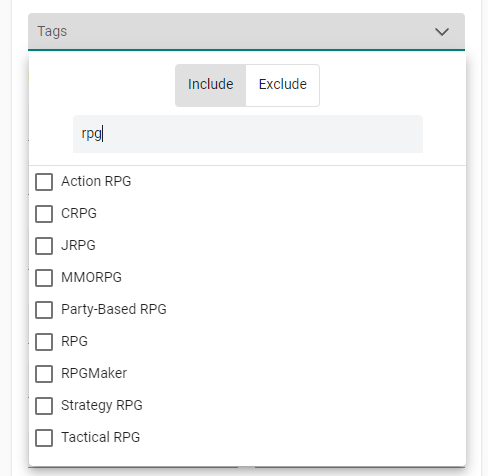

Search for Filters

Some of our filters had tens if not hundreds of options to choose from. We have now added a search bar to make it easier to look for the particular item you’re interested in. For example, you can now find all the RPG tags with ease.